Futures are consolidating yesterdays gains, trading back to 4148. Volatility estimates continue to trend lower as the S&P oscillates in the 4100-4200 zone. Resistance remains at 4200, with support at 4155 (SPY4150), 4127 then a major level at 4100.

As this is the final day of the holiday shortened week, liquidity is still sub-par. Its in environments like this that these outsized, “unreasonably strong” (i.e. no significant catalyst) market moves appear, such as with yesterday and late last week.

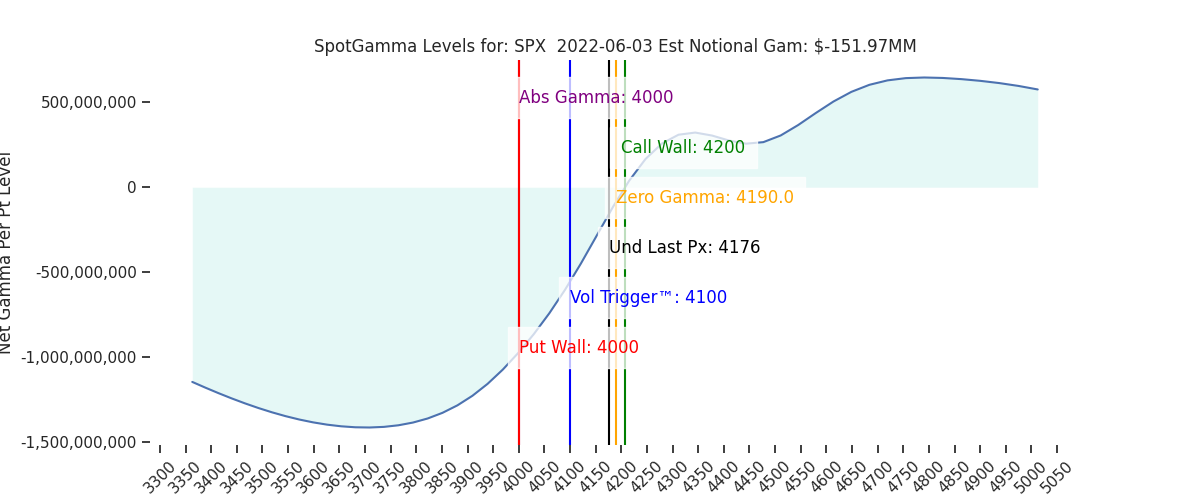

Again, as per last nights note, we saw negative delta trading as the S&P >4150. This is something we’ve seen for several sessions (6/1 PM note), and syncs with the 4200 Call Wall resistance area. As we remain above the Vol Trigger (4100) and below the Call Wall (4200) gamma is weak, and we’d anticipate this wide, range bound trading activity to continue. This weak gamma combining with implied volatility (i.e. VIX) that’s likely at a lower bound, which suggests lower dealer activity.

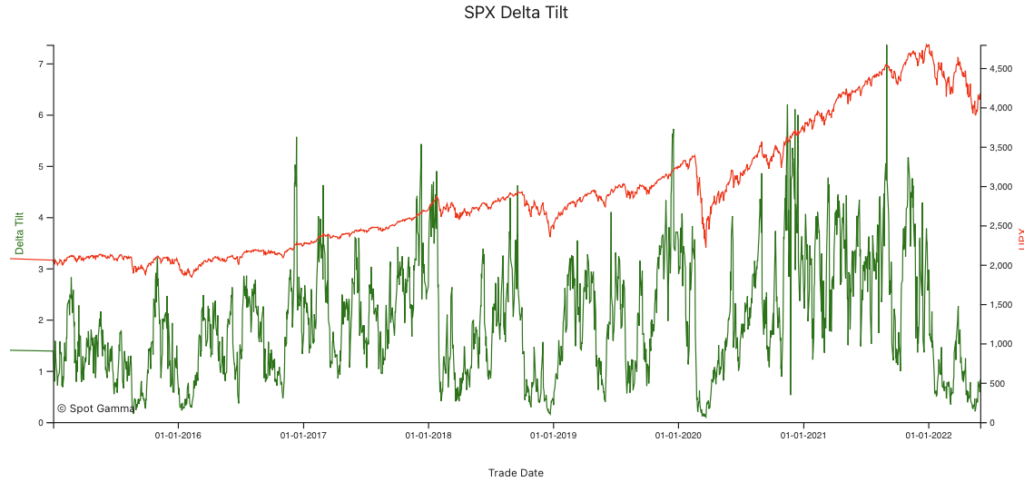

This market still remains very well hedged by large, structural SPX put/VIX Call positions as show below in our Delta Tilt chart. We’ve suggested for several weeks now that traders were given the “green light” to sell short dated volatility. Whats interesting here is that while we do believe there is some of that short vol flow, its been more of a halt in put-buying (we covered this, and the related VVIX collapse here). This has been supportive of “risk on” behavior.

Traders only have one more week of before we hit the big VIX exp/FOMC/OPEX window, and the value of short dated volatility is shrinking. This may mean that speculative “risk on” behavior is likely going to be stifled the closer we get to 6/13, particularly as the options-derived tailwind (gamma, vanna) is shifting to a gentle breeze.

As such, we remain of the opinion that these next few sessions could be an advantageous time to consider some downside insurance. It may be worth looking at options expiring out past June OPEX, as these options will likely hold their value in through FOMC due to the event-vol tied to the 6/15 rate announcements.

Currently our upside target holds at the Call Wall, which is 4200. If the Call Wall rolls up then so does our upside target. Zooming out we continue to watch that 4300 level as an ultimate “best case” upside, due to the large JPM collar put strike (4285) expiring on 6/30.

| SpotGamma Proprietary Levels | Latest Data | Previous | SPY | NDX | QQQ |

|---|---|---|---|---|---|

| Ref Price: | 4176 | 4169 | 417 | 12893 | 314 |

| SpotGamma Imp. 1 Day Move: Est 1 StdDev Open to Close Range | 1.07%, | (±pts): 44.0 | VIX 1 Day Impl. Move:1.55% | ||

| SpotGamma Imp. 5 Day Move: | 2.87% | 4158 (Monday Ref Px) | Range: 4039.0 | 4278.0 | ||

| SpotGamma Gamma Index™: | -0.01 | -0.78 | -0.04 | 0.01 | -0.01 |

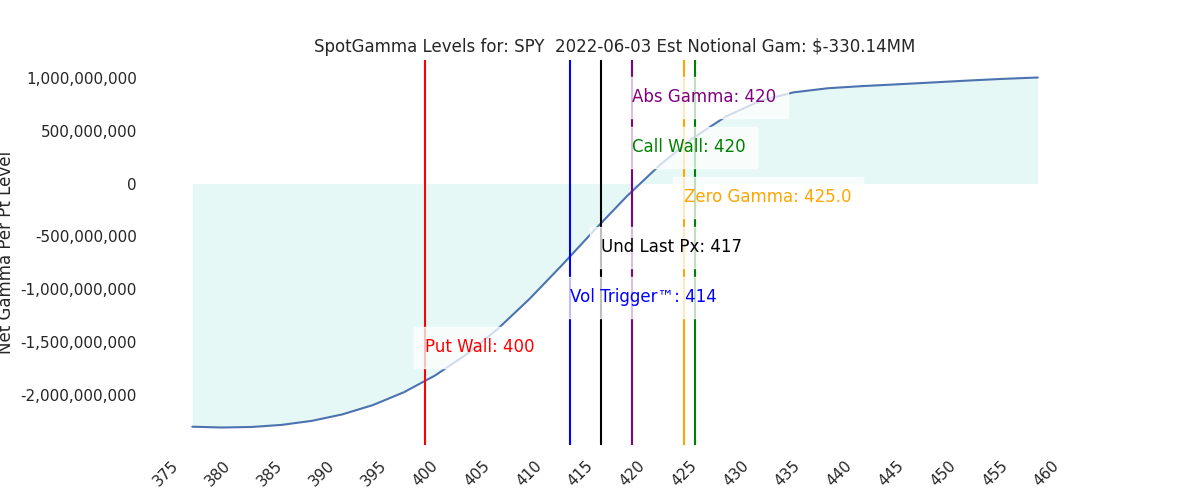

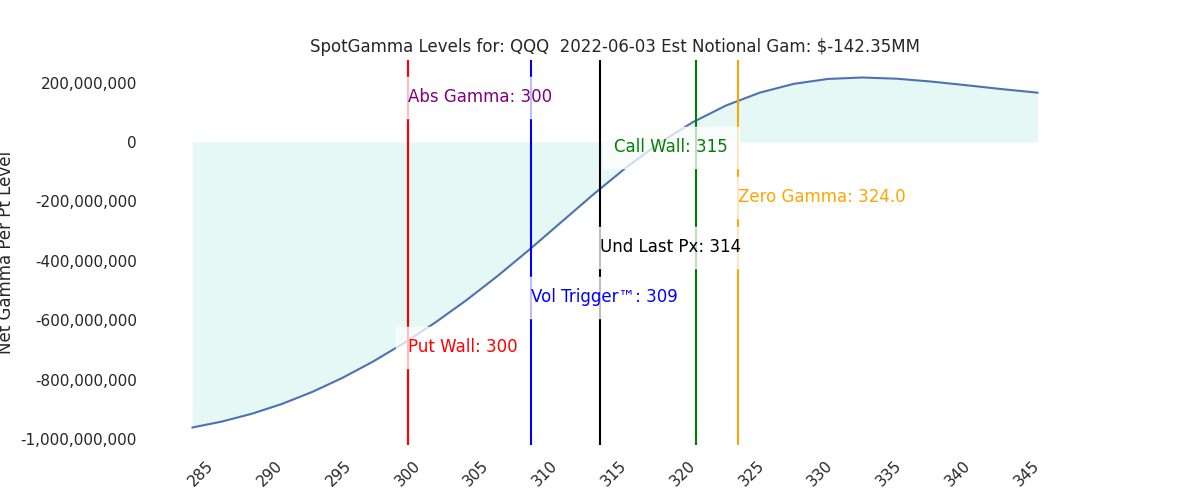

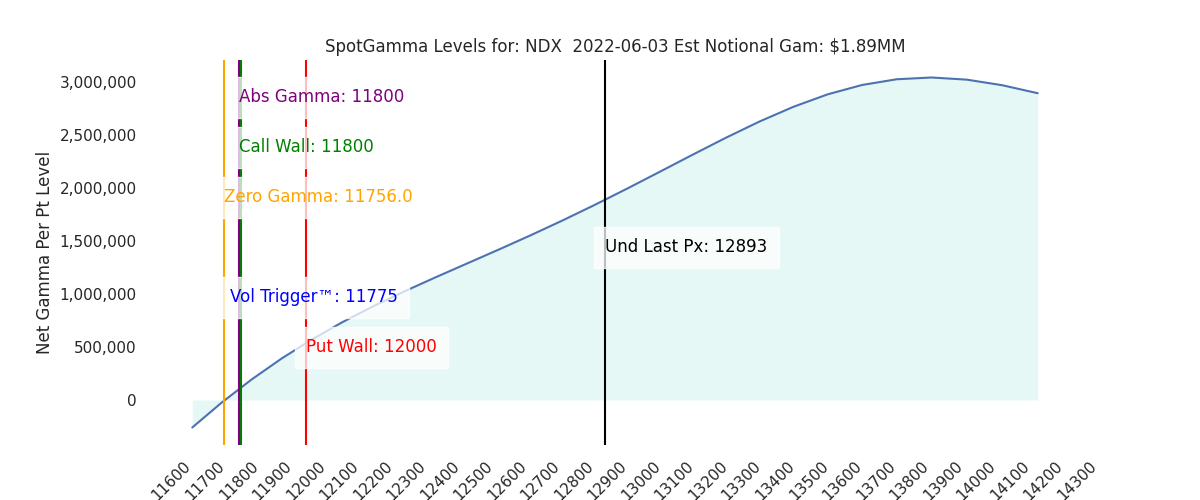

| Volatility Trigger™: | 4100 | 4075 | 414 | 11775 | 309 |

| SpotGamma Absolute Gamma Strike: | 4000 | 4000 | 420 | 11800 | 300 |

| Gamma Notional(MM): | -152.0 | -163.59 | -330.0 | 2.0 | -142.0 |

| Additional Key Levels | Latest Data | Previous | SPY | NDX | QQQ |

|---|---|---|---|---|---|

| Zero Gamma Level: | 4190 | 4214 | 0 | 0 | 0 |

| Put Wall Support: | 4000 | 4000 | 400 | 12000 | 300 |

| Call Wall Strike: | 4200 | 4200 | 420 | 11800 | 315 |

| CP Gam Tilt: | 1.0 | 0.92 | 0.88 | 1.16 | 0.9 |

| Delta Neutral Px: | 4236 | ||||

| Net Delta(MM): | $1,807,570 | $1,779,665 | $180,038 | $62,764 | $118,730 |

| 25D Risk Reversal | -0.07 | -0.08 | -0.06 | -0.07 | -0.07 |

| Call Volume | 463,416 | 379,120 | 2,583,655 | 12,625 | 1,003,215 |

| Put Volume | 756,411 | 873,458 | 3,133,477 | 8,532 | 1,179,252 |

| Call Open Interest | 6,030,533 | 5,867,781 | 6,991,357 | 65,862 | 4,742,729 |

| Put Open Interest | 10,811,687 | 10,611,659 | 11,487,028 | 62,619 | 7,197,538 |

| Key Support & Resistance Strikes: |

|---|

| SPX: [4300, 4200, 4100, 4000] |

| SPY: [430, 420, 415, 400] |

| QQQ: [320, 315, 310, 300] |

| NDX:[14000, 13500, 12000, 11800] |

| SPX Combo (strike, %ile): [4072.0, 4277.0, 4127.0, 4081.0, 4227.0] |

| SPY Combo: [406.96, 427.41, 412.38, 407.79, 422.4] |

| NDX Combo: [12919.0] |