Founder’s Note for: 2023-03-02 06:16 AM EST

Macro Theme: | Key Levels: |

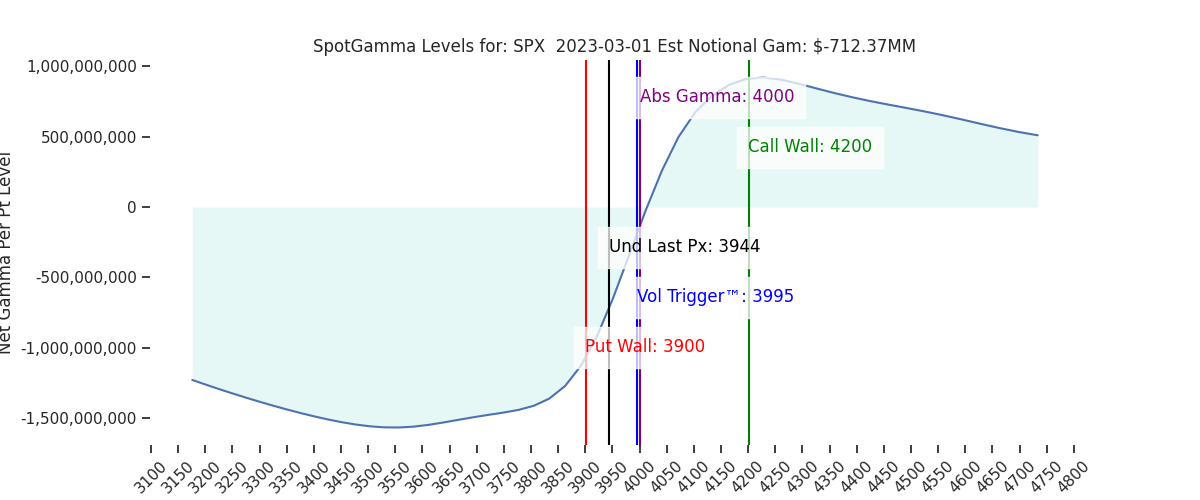

| > Major Resistance: $4,100 > Pivot Level: $4,050 > Critical Support: $4,000 (SPX Large Gamma) > Key Dates: 3/17 OPEX > Major risk lies on a break of 3900, as dealers may flip to negative gamma hedging | Ref Price: 3944 SG Implied 1-Day Move: 0.91% SG Implied 5-Day Move: 2.7% Volatility Trigger: 3995 Absolute Gamma Strike: 4000 Call Wall: 4200 Put Wall: 3900 |

Daily Note:

Futures are lower to 3940, which suggests an implied SPX cash open <3950. We are therefore now watching 3950-3960 (SPY 395) as first resistance, with resistance higher at 3975 & 4000. To the downside, major support is at 3900 (SPX Put Wall). Our model continues to estimate intraday intraday ranges of <=1%, which lines up with the 3900 & 3975 areas.

If the break of 3950 can hold into the cash session, we then give weight to the S&P testing the 390SPY/3900SPX Put Wall. The curveball is 0DTE, which is consistently being used as a mechanism for mean reversion, which in turn suppresses realized volatility. However, we suspect that those flows would now more likely initiate as long delta trades on a test of 3900, which implies 3900 should function as strong support for today. Additionally we would anticipate selling on any rally/retest of the 3975 area.

Whats intersting about 390/3900, is there are mainly net put positions at strikes below. We generally read these areas as having higher volatility. Its therefore in and around this area wherein the idea of the “flow baton” being passed from short dated gamma to longer dated vega occurs. We’ve also characterized this as the “liquidity hole” because in this area we are on watch for implied volatility to jump, which often ties to wider spreads and larger price swings.

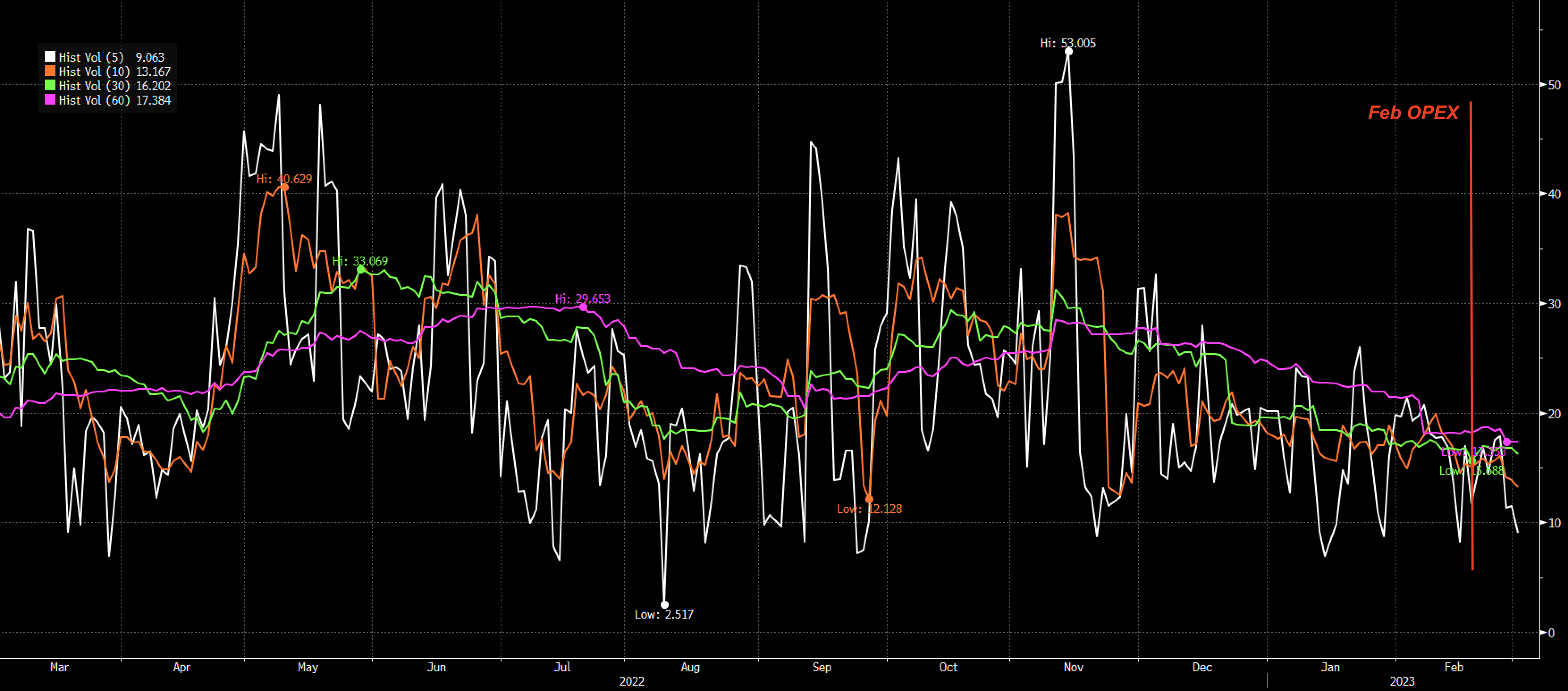

At current levels, the SPX is now down ~5.5% since OPEX week highs, but we reiterate that price action has been a grind. To this point, shown below are various SPX realized vol rolling windows. As you can see they all generally trend lower.

Along with this we see various measures of implied volatility lower, like VOLI, VVIX, SDEX, etc. These are both counterintuitive – one would generally expect more volatility (both IV & RV) with a market that is down 5% in 2 weeks. This relationship isn’t terribly surprising, as one of the core themes of ’22 was volatility “underperforming”.

It is around this aforementioned 3900 level wherein we watch for jump risk, and a short term snap-back in the spot/vol relationship (i.e. vol should spike with market declining).

It’s important to note we have recently been on this precipice, during the first test of 4000, and subsequent test of 3950. Both times, when it looked like IV would finally pop, supportive 0DTE flows came in and open interest quickly built up in the area of weakness (see our note from 2/23). This same setup seems to be in place should markets probe lower, here. With this, we give edge to 3900 holding, and positions filling in around 3900-3950 for tomorrow. This implies “the grind” continues, as the market slowly digests lower prices.

This risk here is on a break of 3900, wherein a break of that level may invoke a surge in volatility.

| SpotGamma Proprietary SPX Levels | Latest Data | SPX Previous | SPY | NDX | QQQ |

|---|---|---|---|---|---|

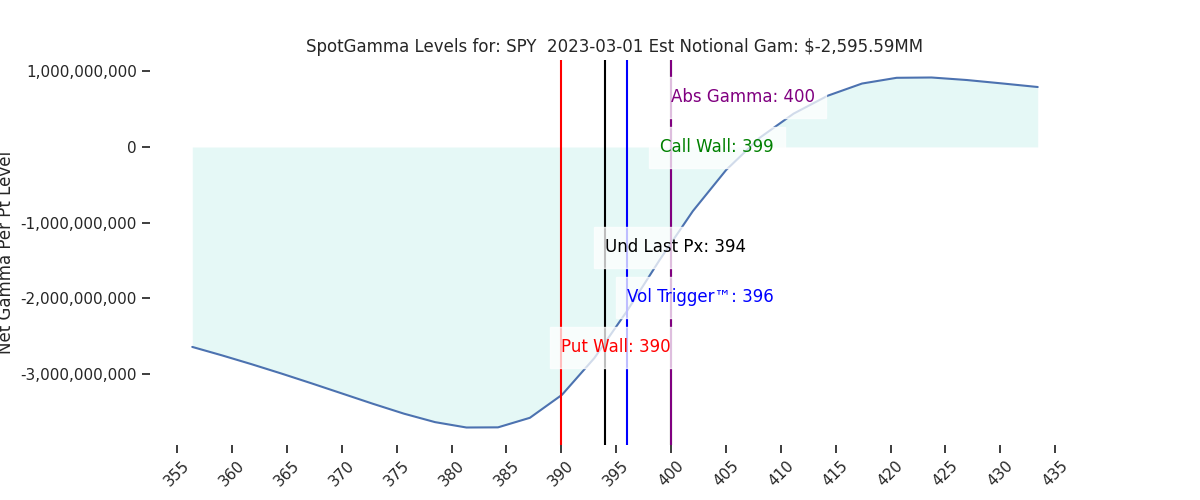

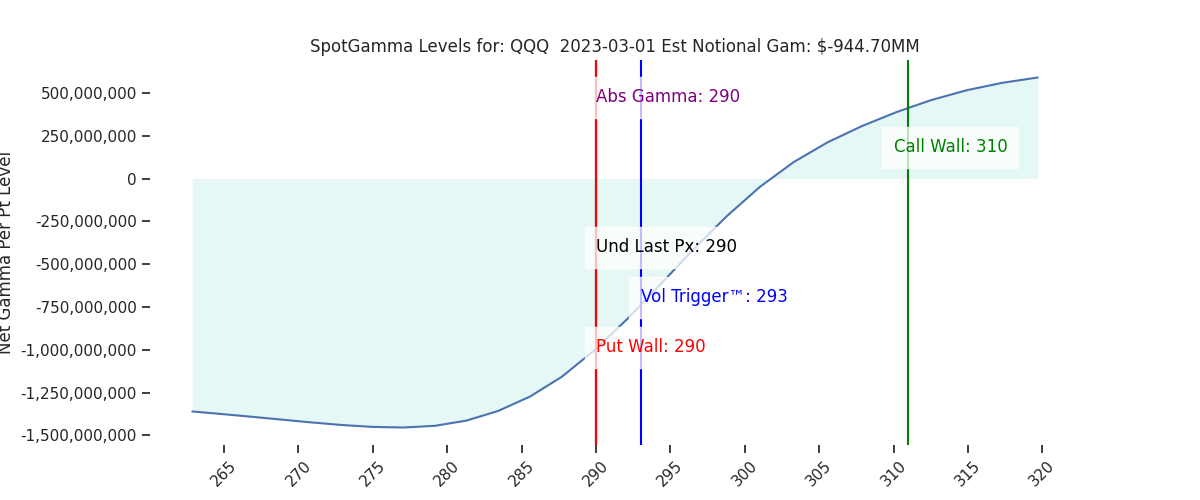

| Ref Price: | 3944 | 3969 | 394 | 11929 | 290 |

| SG Implied 1-Day Move:: | 0.91%, | (±pts): 36.0 | VIX 1 Day Impl. Move:1.3% | ||

| SG Implied 5-Day Move: | 2.7% | 3970 (Monday Ref Price) | Range: 3863.0 | 4077.0 | ||

| SpotGamma Gamma Index™: | -0.90 | -0.92 | -0.43 | 0.03 | -0.10 |

| Volatility Trigger™: | 3995 | 3995 | 396 | 11875 | 293 |

| SpotGamma Absolute Gamma Strike: | 4000 | 4000 | 400 | 12300 | 290 |

| Gamma Notional(MM): | -712.0 | -463.0 | -2596.0 | 5.0 | -945.0 |

| Put Wall: | 3900 | 3900 | 390 | 11000 | 290 |

| Call Wall : | 4200 | 4200 | 399 | 12300 | 310 |

| Additional Key Levels | Latest Data | Previous | SPY | NDX | QQQ |

|---|---|---|---|---|---|

| Zero Gamma Level: | 4016 | 4013 | 405.0 | 11465.0 | 306 |

| CP Gam Tilt: | 0.81 | 0.82 | 0.5 | 1.33 | 0.57 |

| Delta Neutral Px: | 4031 | ||||

| Net Delta(MM): | $1,524,944 | $1,534,497 | $182,216 | $48,206 | $95,098 |

| 25D Risk Reversal | -0.06 | -0.06 | -0.06 | -0.06 | -0.06 |

| Call Volume | 546,550 | 546,550 | 1,817,651 | 7,990 | 595,569 |

| Put Volume | 875,783 | 875,783 | 2,340,397 | 6,894 | 832,625 |

| Call Open Interest | 5,951,626 | 5,951,626 | 6,350,943 | 60,808 | 4,786,014 |

| Put Open Interest | 11,035,950 | 11,035,950 | 13,028,019 | 62,970 | 8,374,298 |

| Key Support & Resistance Strikes: |

|---|

| SPX: [4100, 4000, 3950, 3900] |

| SPY: [400, 398, 395, 390] |

| QQQ: [300, 295, 290, 285] |

| NDX:[13000, 12300, 12000, 11500] |

| SPX Combo (strike, %ile): [(4127.0, 83.06), (4080.0, 79.38), (4044.0, 91.22), (4009.0, 79.93), (4005.0, 78.23), (3938.0, 87.11), (3930.0, 94.51), (3926.0, 78.39), (3918.0, 86.72), (3906.0, 93.76), (3898.0, 87.05), (3886.0, 92.51), (3878.0, 98.56), (3867.0, 79.73), (3855.0, 79.76), (3835.0, 84.3), (3831.0, 92.42), (3788.0, 79.89), (3780.0, 96.36)] |

| SPY Combo: [387.12, 377.26, 392.24, 389.88, 387.91] |

| NDX Combo: [12191.0, 11797.0, 11594.0, 11391.0, 11713.0] |