Macro Theme:

Major Resistance: $4,200

Pivot Level: $4,150

Critical Support: $4,000

Range High: $4,200 Call Wall

Range Low: $3,800 Put Wall

‣ $4,200 is likely heavy resistance into April 21st OPEX

‣ High market volatility is unlikely with SPX >$4,000 due to positive gamma positioning.

‣ 1 Month IV is at lows near 16%, which is likely a long term low which reduces equity vanna tailwinds. It further implies that longer dated IV may be reasonably priced.

Founder’s Note:

S&P futures are flat at 4170 this morning, while NQ futures are -50bps to 13,137. Key SG levels are fairly unchanged with yesterdays move to the large gamma strike of 4150. 4150 – 4160 (SPY 415 Call Wall) is our pivot line for today. First resistance above is at 4171, with 4200 as our maximum high into next weeks monthly expiration. Support is at 4130, then 4110 (SPY 410) – 4100.

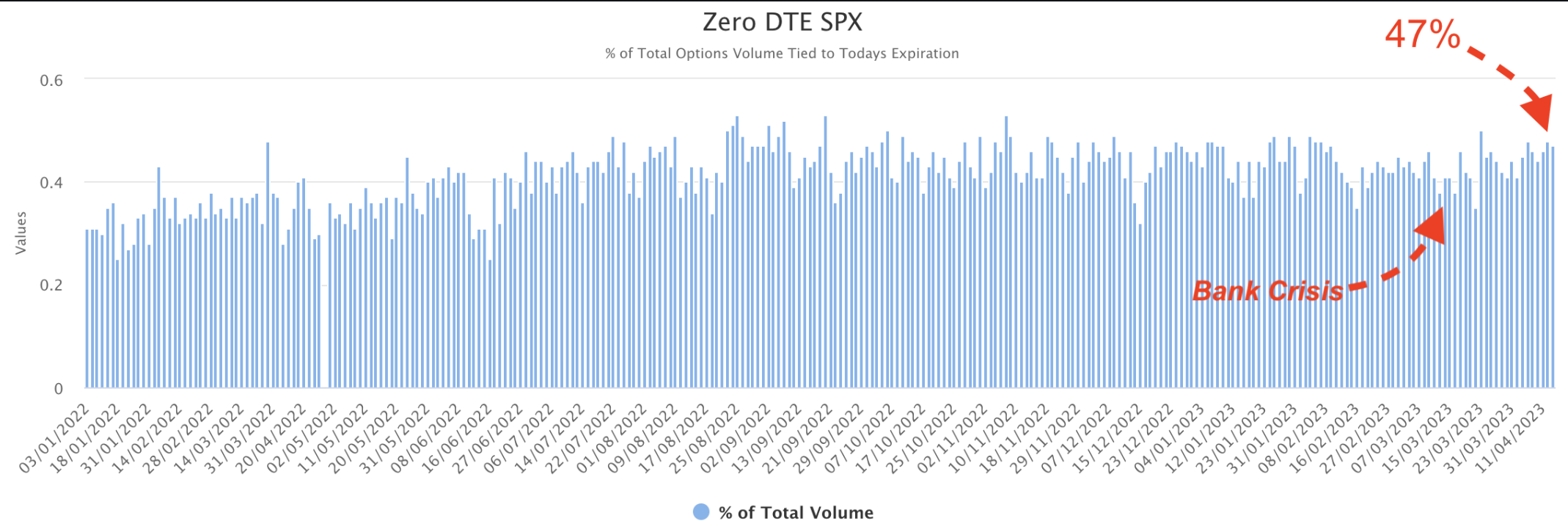

As we discussed in last nights note, yesterdays 0DTE call flow was impressive. Shown below is our HIRO reading for the S&P 500 complex: SPX Index, SPY, and we now include ES futures options. As you can see there is almost no distinction between the green “0DTE call delta”, and “All expiration call delta” (orange) which implies traders focus was indeed on 0DTE. This flow effectively served to move the markets from one large gamma strike (4100) to the next (4150).

47% of yesterdays SPX Index flow was 0DTE which is pressing the high end of historic values (record = 53%). This flow has been increasing over the past several days, and appears to be linked with the reduction in implied volatility. As implied volatility declines, and/or concerns around macro risks fade, 0DTE seems to increase. This was seen during the March banking crisis, wherein 0DTE flows subsided as the VIX spiked >25. We now have a 17-18 handle VIX (i.e. low vol), and a resurgence in 0DTE. The implications of this are that markets are likely to be shoved around by this transient, very short dated order flow, and so longer term conclusions drawn from this price action should be tempered (i.e. “yesterday signaled the start of a new bull market!”).

Because the 0DTE phenomenon, in its current form, only started in Q4 of last year there is not enough data to draw more meaningful correlations between IV & 0DTE. If you are interested in a larger 0DTE discussion, please watch our recent presentation here.

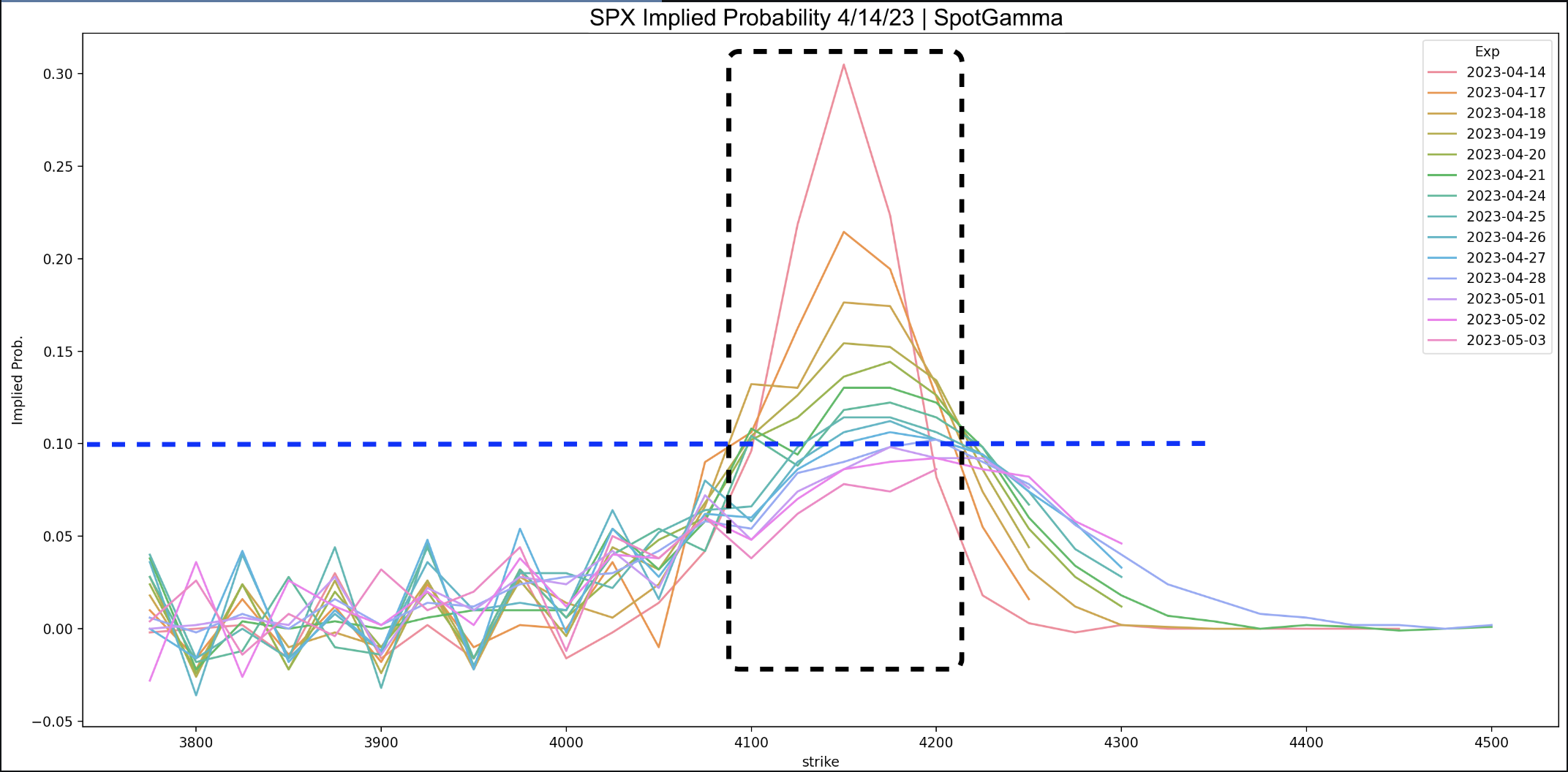

Turning back to yesterday’s rally, it has pushed the market equilibrium >4100 for the next several sessions, vs <4100. Shown below is the implied probability of the S&P closing at various levels by each future expiration. Through this lens we can see that traders are generally pricing in strongest odds of the S&P closing inside of 4100-4200 in through next Friday’s monthly OPEX (4/21). This range coincides with the largest set of positive gamma strikes, which we think should continue to attract/pin markets. We always note the skew of this distribution, as since calls carry a lower IV to puts, the implied odds of a right tail move are relatively lower. This means that traders currently see low odds of a strong move >4200 before next week (red to green lines), whereas there is an extended left tail which suggests “there is always a chance of big moves down”.

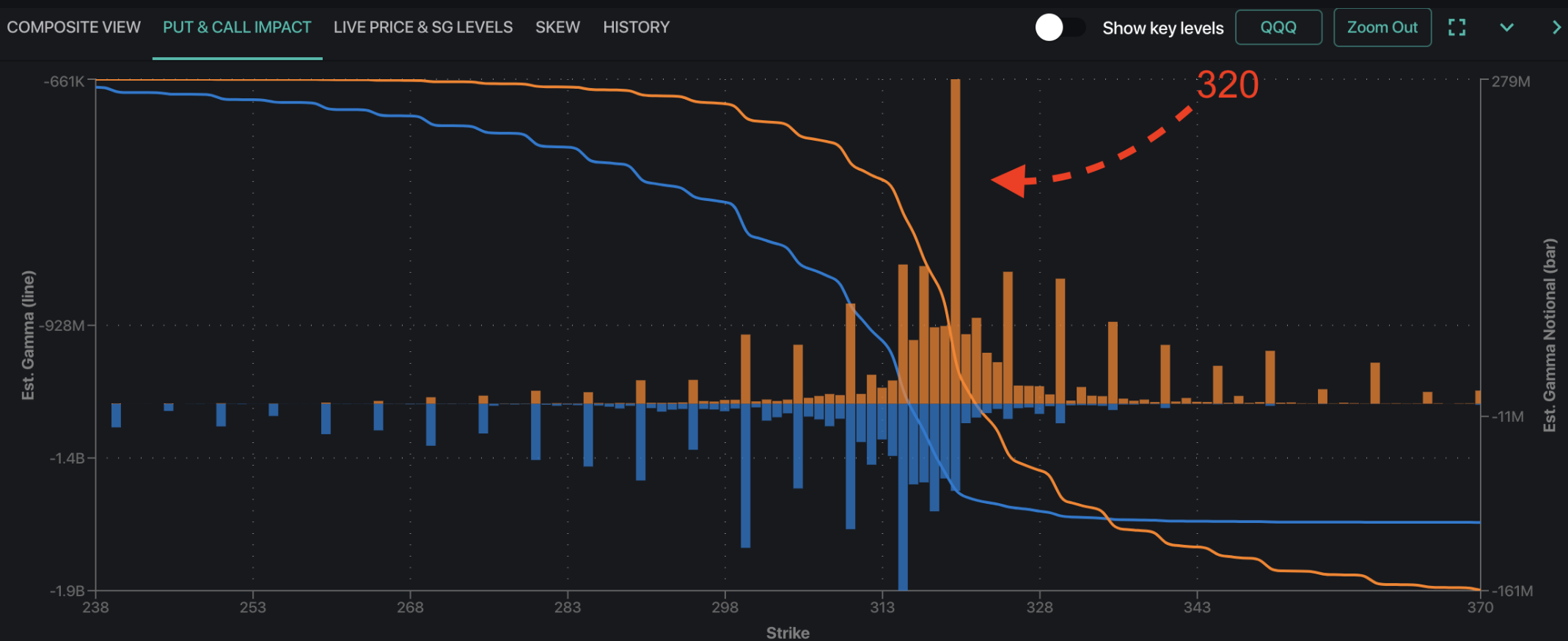

Across to QQQ, we wanted to highlight the very large call strike of 320. As plotted below, that is a very prominent level for the QQQ, and an overhead resistance line that may also serve as significant in through next weeks expiration.

At this point we see little which should impact markets into next week, and continue to look for the “OPEX pin” to hold. There does not appear to be a significant data point, and traders will likely be reluctant to carry large theta bill over the weekend. This should keep IV muted for today, which, along with gamma positioning, plays into tighter trading ranges and mean reversion around large gamma strikes. We think the IV crush into OPEX week is non-random, and would look for a window of IV expansion into the end of April, wherein traders focus will shift to the 5/3 FOMC.

| SpotGamma Proprietary Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Reference Price: | $4146 | $413 | $12848 | $313 | $1796 | $178 |

| SpotGamma Implied 1-Day Move: | 0.94% | 0.94% |

|

|

|

|

| SpotGamma Implied 5-Day Move: | 2.69% |

|

|

|

|

|

| SpotGamma Volatility Trigger™: | $4095 | $411 | $12520 | $315 | $1900 | $177 |

| Absolute Gamma Strike: | $4000 | $410 | $12525 | $315 | $1800 | $180 |

| SpotGamma Call Wall: | $4200 | $415 | $12525 | $320 | $1735 | $178 |

| SpotGamma Put Wall: | $3800 | $400 | $11000 | $300 | $1750 | $170 |

| Additional Key Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Zero Gamma Level: | $4227 | $442 | $12552 | $347 | $1762 | $205 |

| Gamma Tilt: | 1.5 | 1 | 1.7 | 0.91 | 0.66 | 0.62 |

| SpotGamma Gamma Index™: | 1.8 | 0.016 | 0.046 | -0.025 | -0.022 | -0.067 |

| Gamma Notional (MM): | $4.3B | $8B | $29M | $3.5B | $121M | $3.1B |

| 25 Day Risk Reversal: | -5.47% | -4.62% | -5.05% | -5.08% | -4.52% | -4.93% |

| Call Volume: | 558K | 1.9M | 8.7K | 780K | 37K | 196K |

| Put Volume: | 836K | 2.9M | 8.3K | 957K | 47K | 457K |

| Call Open Interest: | 6.1M | 7M | 55K | 4.7M | 174K | 3.3M |

| Put Open Interest: | 12M | 14M | 62K | 8M | 334K | 7.4M |

| Key Support & Resistance Strikes |

|---|

| SPX Levels: [4200, 4150, 4100, 4000] |

| SPY Levels: [420, 415, 412, 410] |

| NDX Levels: [14000, 13000, 12525, 12500] |

| QQQ Levels: [320, 315, 310, 300] |

| SPX Combos: [(4349,89.94), (4325,78.10), (4320,87.69), (4300,97.94), (4291,76.46), (4275,90.23), (4271,75.00), (4250,97.17), (4225,88.22), (4221,79.07), (4213,84.73), (4208,85.92), (4200,99.57), (4192,95.50), (4184,89.78), (4179,87.44), (4175,97.83), (4171,94.66), (4167,87.94), (4163,86.32), (4159,94.55), (4155,86.04), (4150,99.03), (4146,77.69), (4138,83.99), (4130,89.67), (4125,86.32), (4051,78.98), (4009,80.21), (4001,89.29), (3951,86.02)] |

| SPY Combos: [418.66, 413.76, 388.87, 408.87] |

| NDX Combos: [12527, 13131, 12309, 13337] |

| QQQ Combos: [317.1, 302.39, 327.12, 322.11] |