Macro Theme:

Short Term SPX Resistance: 4,800

Short Term SPX Support: 4,700

SPX Risk Pivot Level: 4,700

Major SPX Range High/Resistance: 4,800

Major SPX Range Low/Support: 4,500

‣ We look for higher volatility (i.e. more market movement) starting this week (12/18), out of the huge 12/15 OPEX.*

‣ 4,800 is our current max upside target, due to a Call Wall shift on 12/19. Call Walls in QQQ/IWM are at 410/205.*

‣ A downside break of 4,700 is our interim “risk off” level.*

‣ January OPEX is setting up to be a major event, with a risk that expiring large long call positions could pull markets lower mid to late January.*

*updated 12/20

Founder’s Note:

ES Futures are up 50bps to 4,774. Key SG levels for the SPX are:

- Support: 4,700, 4,689, 4,664

- Resistance: 4,727, 4,750, 4,764, 4,775, 4800

- 1 Day Implied Range: 0.79%

For QQQ, support is at 405, with resistance at 410.

In IWM, support is at 195, with resistance at 197 & 200.

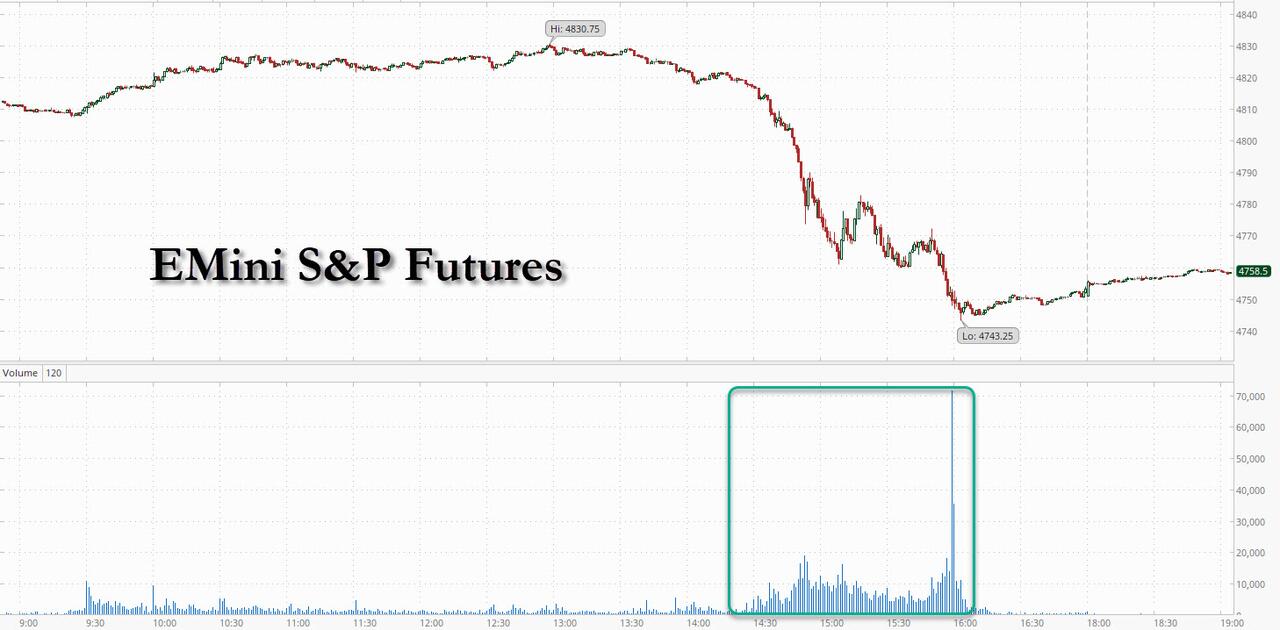

Yesterday had a lot of the elements of a flash crash, as the only apparent trigger of downside action were the flows that caused them.

Heading into last nights 1pm ET treasury auction, our

HIRO

readings were +$4bn on the day, and after that auction the negative deltas began to build. The first wave was call selling (red box), and the second wave was put buying (yellow box). In both cases the flow was predominantly 0DTE flow (we can tell because the spread between 0DTE lines and All Exp lines stays equidistant), and the end result of this is a lows of

HIRO

are -$3bn around 3pm ET. Therefore that is roughly $7bn of S&P500 deltas dumped in about an hour – but that’s just S&P500. As we chronicled last night, Mag7 added another ~$1.5 billion of negative deltas.

Heading into this drawdown, ATM IV’s were <=8% (based on start of day), suggesting that traders were pricing in only ~50bps of movement in the S&P500. Therefore, as soon as the put buying picked up at 2:30PM, there seemed to be a scramble for negative 0DTE delta (i.e. put buying).

Whats interesting about this, is that its right after 2:30PM ET that selling in the ES picks up. Whether this was a hedging response to those negative

put deltas

, or flow that coincided with it, the market pressure was likely the same. In either case, we are labeling yesterdays move as a “mini flash crash”.

From ZH (emphasis theirs): As Goldman’s Washington explains, while we have seen passive selling over the past few days, “it clearly is not enough to cause such a swift reversal intraday.” Looking at S&P E-Mini’s, most volume started printing after 2:30pm, even prior to the break of 4800 and the pickup in volume was real. The average run rate over the 45 minutes following the initial move was ~5x greater than earlier in the cash session.”

How does this impact things moving forward?

Anytime we see flows that are 0DTE driven, we favor fading those moves. Further, the flows shut off right as the S&P500 hit our critical “risk off” support line of 4,700.

Additionally, yesterday served to pump up implied vols, shown by the VIX which jumped to 13.4. However, when you look under the hood the volatility change out past this week (below the red box) represents a shift just off of “not a care in the world”. This weeks IV’s are a bit more responsive (i.e. brighter green), but that makes sense given yesterday’s surprise 1-1.5% equity tanking.

We can’t help but give edge to this elevated vol getting sold into the upcoming holiday weekend, and into New Years. This should create some recovery for equities today & tomorrow, and we wouldn’t be surprised if we re-tag yesterdays highs. A break of 4,700 remains risk off, wherein selling likely shifts towards longer term flows.

Note that traders are watching today’s 8:30AM ET GDP print, and tomorrow’s core PCE, but we think that odds are they ultimately do not matter much (barring sharp misses).

| SpotGamma Proprietary Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Reference Price: | $4698 | $468 | $16554 | $403 | $1982 | $196 |

| SpotGamma Implied 1-Day Move: | 0.79% | 0.79% |

|

|

|

|

| SpotGamma Implied 5-Day Move: | 2.00% |

|

|

|

|

|

| SpotGamma Volatility Trigger™: | $4710 | $469 | $16275 | $405 | $1935 | $197 |

| Absolute Gamma Strike: | $4700 | $470 | $16650 | $400 | $2000 | $195 |

| SpotGamma Call Wall: | $4800 | $475 | $16650 | $410 | $2005 | $200 |

| SpotGamma Put Wall: | $4695 | $465 | $16000 | $403 | $1800 | $170 |

| Additional Key Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Zero Gamma Level: | $4671 | $467 | $15547 | $402 | $1934 | $193 |

| Gamma Tilt: | 1.069 | 0.846 | 1.686 | 0.883 | 1.116 | 1.096 |

| SpotGamma Gamma Index™: | 0.409 | -0.17 | 0.060 | -0.05 | 0.006 | 0.013 |

| Gamma Notional (MM): | ‑$129.248M | ‑$293.775M | $7.935M | ‑$149.786M | $6.53M | $188.669M |

| 25 Day Risk Reversal: | -0.021 | -0.012 | -0.013 | -0.011 | -0.005 | 0.009 |

| Call Volume: | 633.101K | 2.593M | 21.696K | 963.951K | 37.273K | 815.227K |

| Put Volume: | 1.116M | 3.624M | 21.052K | 1.185M | 59.898K | 807.931K |

| Call Open Interest: | 6.291M | 6.944M | 47.825K | 3.715M | 196.754K | 4.267M |

| Put Open Interest: | 11.881M | 12.47M | 53.619K | 6.742M | 348.916K | 7.007M |

| Key Support & Resistance Strikes |

|---|

| SPX Levels: [5000, 4700, 4650, 4600] |

| SPY Levels: [475, 470, 465, 460] |

| NDX Levels: [17000, 16650, 16500, 16000] |

| QQQ Levels: [405, 404, 403, 400] |

| SPX Combos: [(4900,96.15), (4877,81.64), (4849,95.55), (4825,88.98), (4821,74.23), (4816,89.30), (4811,78.45), (4802,99.33), (4797,73.78), (4792,79.30), (4778,92.32), (4774,93.46), (4769,77.21), (4764,93.40), (4759,78.79), (4750,97.69), (4736,91.89), (4731,86.01), (4727,95.37), (4708,87.02), (4703,78.95), (4694,98.46), (4689,97.37), (4684,96.66), (4680,81.00), (4675,95.89), (4670,91.06), (4665,96.10), (4661,72.13), (4656,73.60), (4647,83.86), (4637,73.67), (4614,74.50), (4548,77.35), (4525,75.98), (4501,93.07)] |

| SPY Combos: [473.15, 470.8, 475.03, 470.33] |

| NDX Combos: [16653, 16836, 16554, 16504] |

| QQQ Combos: [402.01, 406.88, 411.75, 417.03] |

SPX Gamma Model

View All Indices Charts