Macro Theme:

Short Term SPX Resistance: 4,800

Short Term SPX Support: 4,750

SPX Risk Pivot Level: 4,700

Major SPX Range High/Resistance: 4,800

Major SPX Range Low/Support: 4,500

‣ 4,800 is our current max upside target, due to a Call Wall shift on 12/19. Call Walls in QQQ/IWM are at 414/205.*

‣ A downside break of 4,700 is our interim “risk off” level.*

‣ SPX IV’s for the final week of 2023 are extremely low, and we warn traders of “jump risk” embedded with this (see note).*

‣ January OPEX is setting up to be a major event, with a risk that expiring large long call positions could pull markets lower mid to late January.*

*updated 12/27

Founder’s Note:

ES Futures are down 50bps to 4,795. Key SG levels for the SPX are:

- Support: 4,700

- Resistance: 4,750, 4770, 4,800

- 1 Day Implied Range: 0.75%

For QQQ support is at 407 & 405, with resistance at the 409

Call Wall.

In IWM, support is at 194, with resistance at 200, and the 205

Call Wall.

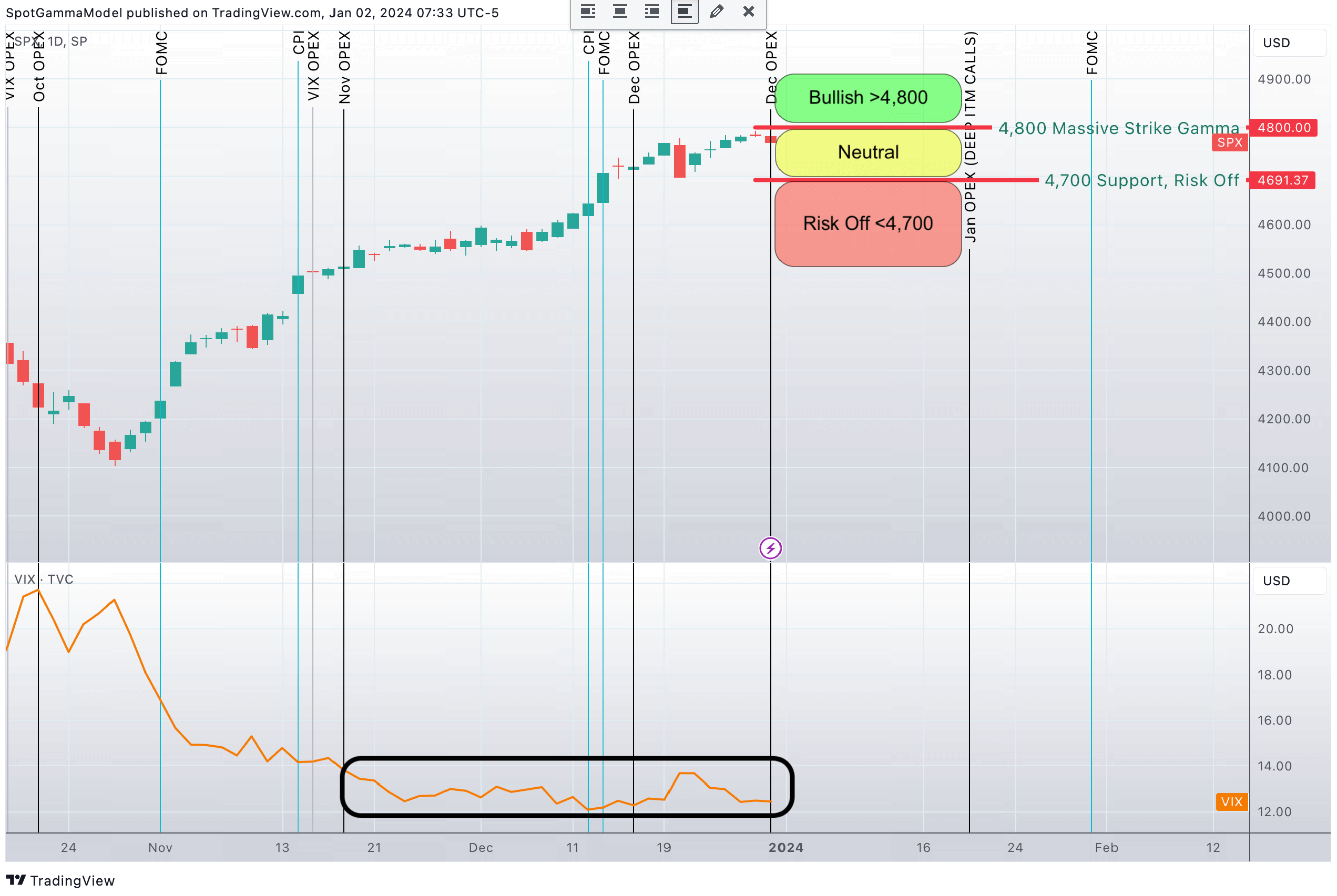

We kick off 2024 with a recap of the current situation:

- The S&P500 & Nasdaq closed 2023 ~1% from all time highs

- Realized volatility [RV] is quote low, with 1-month SPX RV at 9%. These are the lowest levels of RV since late ’21

- 1-month ATM Implied vols [IV] are near 11%, which, given the low RV, is generally fairly valued

- IV for downside strikes (i.e. puts) are quote low suggesting traders are not positioned for risk-off

- There is a massive January expiration on 1/19, which we believe is a catalyst for volatility

- The Jan FOMC is on 1/31

The summary of this is that traders have been enjoying strong equity performance, which has resulted in a drop of volatility expectations (the recent past is the basis for the future). This has also likely drawn out put sellers, emboldened by the success of being short puts since Nov 1 FOMC, with the SPX +13% since that date.

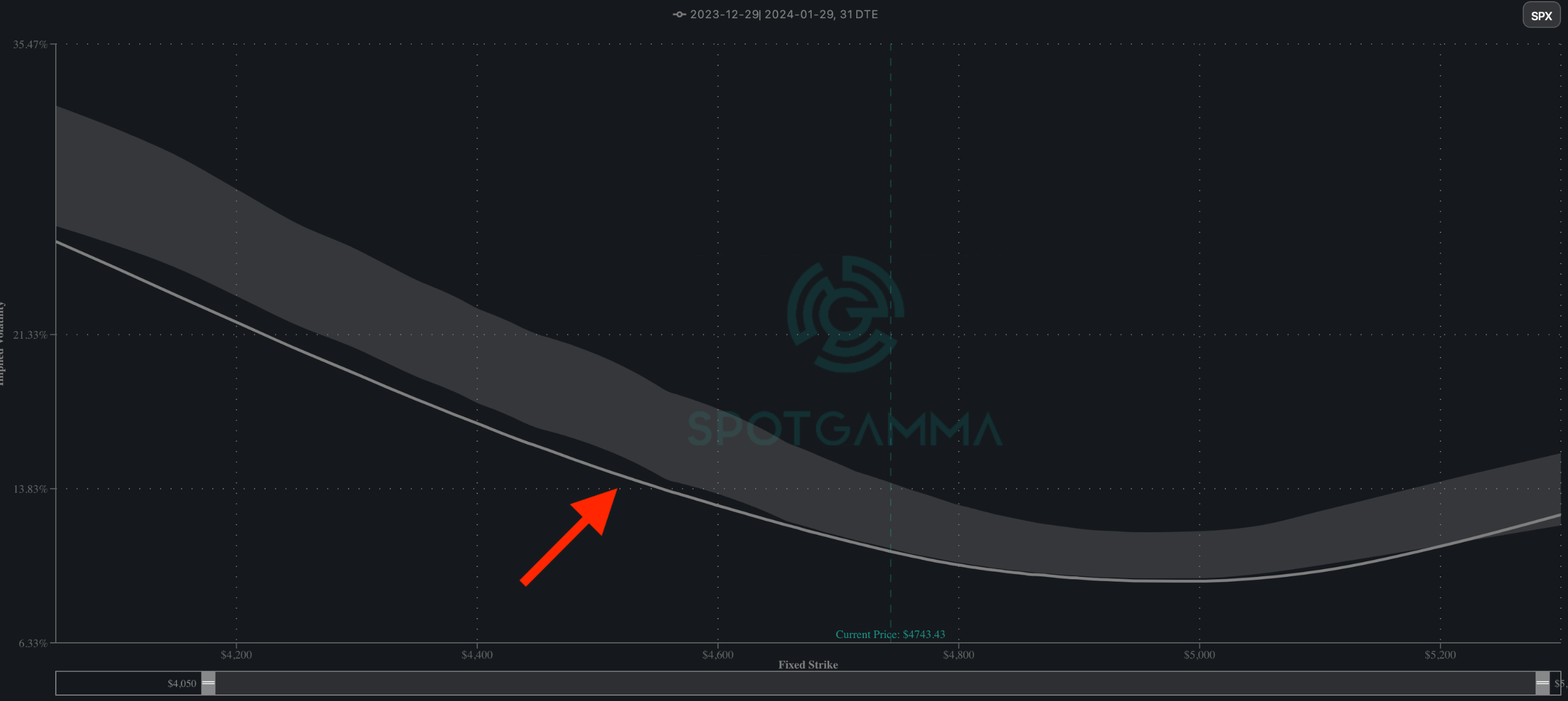

Below we have 1 month skew (1/19 exp) which frames the volatility landscape. Current IV’s are at or below the shaded 10-90% percentile range, implying that IV’s are lower than most readings for the last 60 days. This is particularly true to the downside (red arrow), but now appears to the upside, too. The upside is notable because it was only a few weeks ago that there was a demand for upside calls, that was lifting index call IV/skew. That has dried up as the S&P moved into 4,800.

What is so important about 4,800?

Gamma by strike is shown below, and as you can see, 4,800 is very large. This strike has been quite large since positions rolled at the 12/15 OPEX, with the S&P making an intraday high 4,792 on the 28th. When you couple the growth of this strike in gamma terms with the decline of call skew (above), it appears call sellers have been stepping up of late. While this IV crush is/was over the last two, holiday-laden weeks, we see traders starting this year pricing low volatility out in time, meaning the volatility crush has not been limited to short dated expirations.

Also make note of the large 5,000 strike, and 4,700 level, below as we will touch on them below.

We have distilled positioning down into the following map, which should take us through to January 19th OPEX.

First, to the upside, if the S&P can digest the 4,800 strike and move above it, 4,800 should then serve as solid support. We’d therefore be constructively bullish >4,800 with a target of 5,000. That 5k strike, shown above, has been gaining is size into the end of ’23. While we believe much of that 5k strike position started as box spread financing trades, it does appear that some longer dated calls have been added to that level. This, we think, makes the 5k level a strong attractant if the SPX moves higher >4,800.

Given we start the year with ES futures -50bps, traders may be now starting to examine prospects for risk-off. Our view has been that any test of 4,700 is simply a phase of bullish consolidation, but a break <4,700 opens the door for a much more volatile scenario.

Why 4,700? First, the balance of gamma shifts from calls, to puts. While this balance is technically measured by the Vol Trigger (4,770), its <4,700 where the gamma becomes more materially negative. This suggests that dealer hedging flows may shift from working to suppress volatility, to hedging in ways that exacerbate volatility.

Second, is the impact of IV & vanna. Current IV metrics, framed by the top chart of 1/29 EXP skew, informs us that traders are not positioned for downside risk (i.e. they are likely short puts). Any downside break would therefore likely lead to a cover of those puts, as well as incremental long put demand. If IV pops higher, put prices jump, which should require downside hedging (i.e. larger negative delta) from the dealer community. This larger negative delta due to a spike in IV is the vanna component.

This brings us to the final important aspect of options positioning: the January OPEX.

As we discussed last week, we have a theory that 0DTE options have been reducing volatility around large index expiration. However, this January expiration is driven by very large, deep in-the-money call options in single stocks. These positions are likely hedged out with dealer long delta positions (i.e. long stock), and should the market start to drop dealers may have to start selling stock. Further, because these positions expire in a few weeks, those that are long these valuable calls may elect to close and/or roll them if markets start to decline. The act of closing and/or rolling out these calls should create a long delta imbalance for dealers, which could result in them selling stock.

This position is larger than that of Jan ’22, wherein the S&P lost ~12% over the first 3 weeks of the month, bottoming the day after options expiration. While we are not here to predict a similar drawdown this month, we are here to flag the embedded risks should the S&P break 4,700. In this scenario we do not have a downside price target, as much as a downside time-frame (i.e. down into Jan OPEX).

| SpotGamma Proprietary Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Reference Price: | $4769 | $475 | $16825 | $409 | $2027 | $200 |

| SpotGamma Implied 1-Day Move: | 0.75% | 0.75% |

|

|

|

|

| SpotGamma Implied 5-Day Move: | 2.08% |

|

|

|

|

|

| SpotGamma Volatility Trigger™: | $4770 | $474 | $16425 | $408 | $1920 | $199 |

| Absolute Gamma Strike: | $4800 | $475 | $16650 | $409 | $2000 | $200 |

| SpotGamma Call Wall: | $4850 | $480 | $16650 | $409 | $2005 | $205 |

| SpotGamma Put Wall: | $4600 | $450 | $14500 | $407 | $1700 | $194 |

| Additional Key Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Zero Gamma Level: | $4742 | $471 | $15802 | $408 | $1962 | $197 |

| Gamma Tilt: | 1.15 | 1.176 | 1.932 | 1.064 | 1.171 | 1.211 |

| SpotGamma Gamma Index™: | 0.775 | 0.163 | 0.082 | 0.041 | 0.009 | 0.026 |

| Gamma Notional (MM): | $321.433M | $576.669M | $9.929M | $240.723M | $9.155M | $266.571M |

| 25 Delta Risk Reversal: | -0.025 | -0.02 | -0.026 | -0.026 | -0.017 | -0.016 |

| Call Volume: | 572.032K | 1.791M | 11.322K | 1.145M | 13.698K | 515.159K |

| Put Volume: | 1.082M | 2.385M | 15.359K | 1.646M | 25.278K | 608.973K |

| Call Open Interest: | 5.899M | 6.476M | 50.184K | 5.516M | 210.281K | 4.256M |

| Put Open Interest: | 11.495M | 11.308M | 60.365K | 9.535M | 370.044K | 7.121M |

| Key Support & Resistance Strikes |

|---|

| SPX Levels: [5000, 4800, 4750, 4700] |

| SPY Levels: [480, 477, 476, 475] |

| NDX Levels: [17000, 16650, 16500, 16000] |

| QQQ Levels: [410, 409, 408, 399] |

| SPX Combos: [(4999,98.04), (4951,92.29), (4927,84.45), (4918,75.70), (4899,98.70), (4875,90.76), (4865,74.34), (4851,98.96), (4841,72.60), (4837,72.56), (4832,80.62), (4827,96.23), (4822,79.52), (4818,93.79), (4808,90.85), (4798,97.19), (4794,84.40), (4784,87.70), (4775,95.87), (4746,85.59), (4736,81.30), (4717,77.17), (4708,75.98), (4651,77.76), (4598,92.39), (4550,82.73)] |

| SPY Combos: [479.05, 497.13, 477.15, 482.38] |

| NDX Combos: [16658, 16809, 16927, 17011] |

| QQQ Combos: [403.91, 412.93, 407.6, 408.83] |

SPX Gamma Model

$3,841$4,341$4,841$5,724Strike-$1.5B-$798M-$98M$1.1BGamma NotionalPut Wall: 4600Call Wall: 4850Abs Gamma: 4800Vol Trigger: 4770Last Price: 4769

View All Indices Charts