Macro Theme:

Short Term SPX Resistance: 4,770

Short Term SPX Support: 4,720

SPX Risk Pivot Level: 4,700

Major SPX Range High/Resistance: 4,815 (SPY Call Wall)

Major SPX Range Low/Support: 4,600

‣ 4,800 – 4,815 is our current max upside target into 1/19 OPEX. Call Walls in QQQ/IWM are at 409/200.*

‣ A downside break of 4,700 is our interim “risk off” level.*

‣ January OPEX is setting up to be a major event, with a risk that expiring large long call positions could pull markets lower mid to late January.*

‣ Implied volatility remains muted despite recent equity market weakness, with a surge in demand for long volatility (i.e put buying) is a potential driver of equity weakness.*

*updated 1/16

Founder’s Note:

ES Futures are down 30 to 4,787. Key SG levels for the SPX are:

- Support: 4,750, 4,720, 4,700

- Resistance: 4,770, 4,800 SPX

Call Wall,

4,815 SPY Call Wall

- 1 Day Implied Range: 0.68%

For QQQ:

- Support: 405, 402, 400

- Resistance: 410

IWM:

- Support: 190, 185

- Resistance: 194, 200

GS and MS report this morning, around 7:30 AM ET.

TLDR: SPX upside appears to have major resistance at the 4,800-4,815

Call Wall

band (SPX, SPY Walls), and this likely holds into Friday OPEX. To the downside we see 4,700 SPX as major support, but <4,700 remains a major risk-off level for the reasons outlined below. We think a large downside move is a legitimate risk this week, due to the large Jan OPEX.

While we risk sounding like the “Boy Who Cried Wolf” on the risk-off front, we must continue to highlight two key issues with this market:

- The very large, deep ITM calls set to expire on Friday, 1/19

- The low implied volatility levels

Let’s start with the latter. Heading into the weekend, S&P500 IV’s were generally near multi-year lows as evidenced by the 12-handle VIX. These low VIX readings were not particularly unreasonable given that SPX 1-month volatility is also at multi-year lows, near 10%.

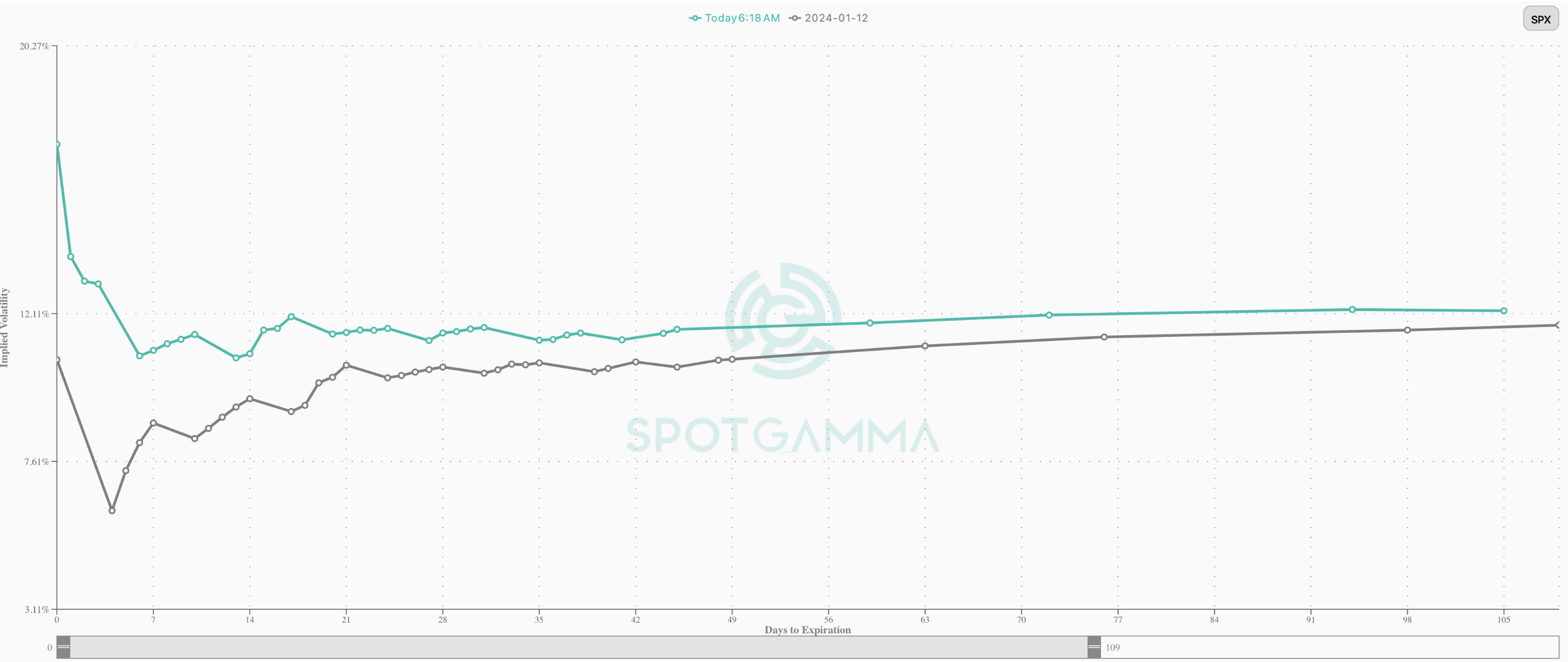

This morning, with ES futures down 60bps, we see that IV’s are perking up, with the VIX at 14. You can also see these higher IV’s in the SPX term structure, shown below, with Friday’s reading (gray) vs this AM’s reading (green). These aren’t exactly “hot” IV readings, as very short ATM IV’s are in the low teens, implying ~80bps daily SPX moves. These values, however, appear a bit higher than simple mean reversion from Friday’s pre-holiday-weekend lows.

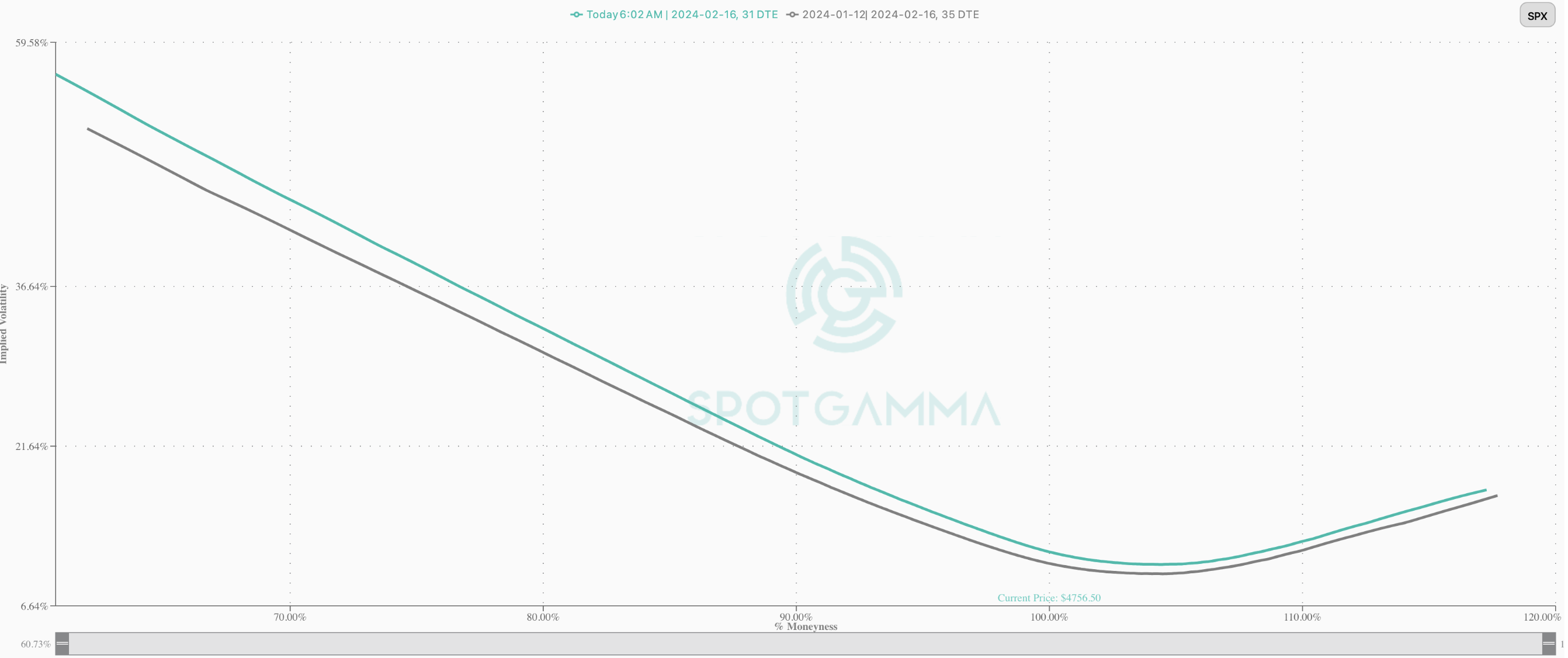

Looking at some skew metrics, we’ve plotted 1-month SPX IV’s below. As you can see, there is about a 1-1.5 vol point shift between the Feb 16th (monthly) OPEX readings from Friday (gray) vs this AM (green). This is what one would anticipate with futures off 60bps.

The point here is that the volatility pump is priming, but we’ve seen this action a few times over the past few weeks during bouts of equity weakness. However, each time it has appeared a larger vol spike is imminent, (vol) sellers have stepped in, and equities rapidly recovered.

This “priming”, or first move, is important as it builds some energy/vanna up in the equity eco-system. The risk here is that, with equities indexes just off of all time highs, volatility is not priced for any type of major move lower. A bid to volatility would press equity weakness.

Further, through a bearish lens, there is plenty of upside to volatility, and this early move may be nudging vol sellers from last week offsides. If they percieve this downside move as “real”, they may then elect to cover their shorts, which may jump the vol move up.

We’d interject here that recently when we’ve seen equities leak lower, a big 0DTE bid comes in (more on this below).

Conversely, there is now some volatility premium that vol sellers may look to extract. If those vol sellers come out, it can quickly lead to mean reversion in equities, back to Friday’s closing levels. We’d anticipate that any rally attempt would stall out into the major 4,800-4,815 level.

The tipping point (aka the downside is “real” this time”), remains 4,700. We have thought, and continue to think, that <4,700 sparks a reflexive move that pushes equities lower, and IV meaningfully higher.

This takes us to the second part of this reflexive downside response, and the large Jan OPEX. We’ve covered this ad nauseam, but we continue to think the risk of an OPEX unwind is real. Should equities start to slide, long stock hedges tied to deep ITM call positions may have to be unwound in kind. This too could speed up a downside slide in equities. There was a similar setup in Jan ’22 which dropped the SPX -6% over the same OPEX week.

For more on this, please see this note, and/or last Thursday’s Member webinar.

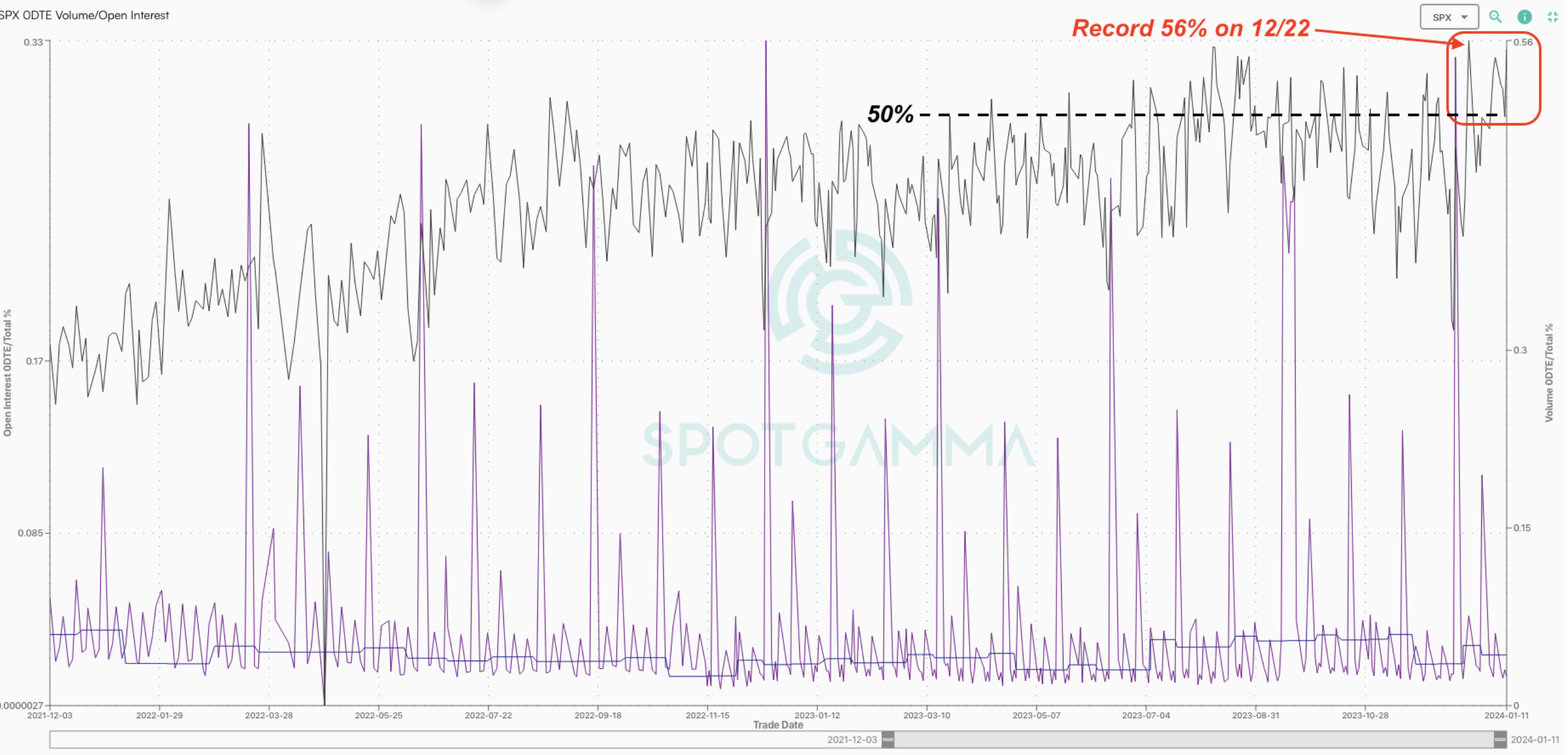

Lastly, we wanted to cover 0DTE. We’ve seen some recent interviews with industry folks which have made light of the attention on 0DTE, and actually poked fun at those that think there is a potential risk in these contracts. What’s ironically seemed to happen into these remarks, is that 0DTE use is increasing. Shown below is SPX 0DTE volume percentage, and as you can see we’ve sustained >=49.7% over the last week, nearly breaking the 0DTE volume percent record of 56% from 12/22.

We also flag this recent data from the OCC, which informs us that last week featured the most Index options contracts bought to open – ever (bottom chart, blue line). The OCC does not break this data down by underlying nor tenor, but we know that SPX trading dominates Index option volumes. Further, we can compare the record setting contract volume vs only average premiums purchased over the same period (top). Since 0DTE contracts are have the lowest nominal value, we can infer that this data is reflecting 0DTE contracts as spurring this record contract buying.

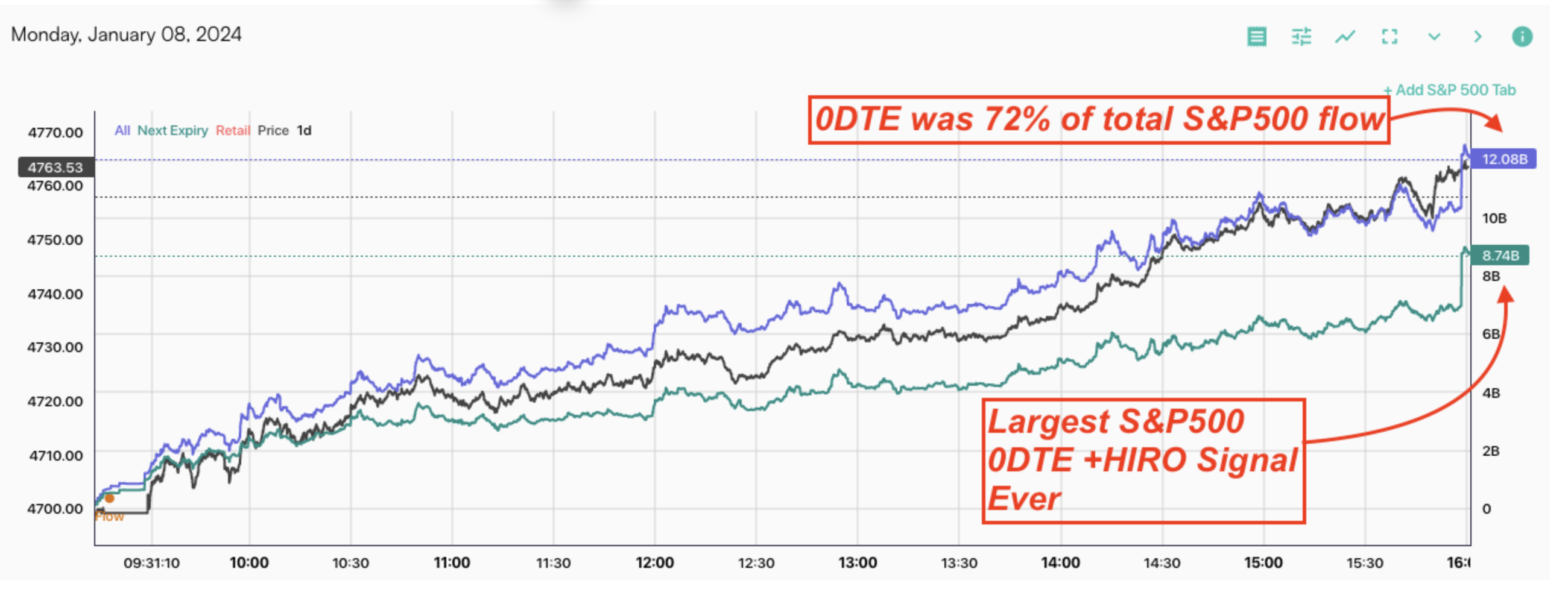

Lastly, we recorded our largest ever positive

HIRO

reading last Monday (1/8) of $12bn, of which 72% was 0DTE. These were massive flows, and on this day the SPX rallied 1.2% from 4,700 lows. We speculate that, on weakness, these buyers are trading 0DTE for both hedging & speculation, using both call buying and/or put selling. This flow promotes mean reversion in equities. Whats interesting is that this flow appears into equity market weakness, but dries up as the SPX rallies into 4,800. This implies 0DTE may be more hedging flow, vs speculation.

The argument with 0DTE is that 0DTE traders/exposure are hedged out with other 0DTE contracts, and so there is no impact to the underlying equity market. We think there are a variety of scenarios in which this argument can fall apart, and the trading of 0DTE can lead directly to underlying market impact.

Consider, for example, if Market Maker A [MMA] sells 100 contracts to a retail trader. They then buy 100 contracts at a higher price, to hedge their exposure. Odds are, they’d have to buy those “higher priced” contracts from Market Maker B [MMB]. MMB now has short upside exposure, and so you could end up with this daisy-chain of rolling exposure as MMB looks to hedge their exposure. During markets which remain inside of implied moves this is all likely not an issue, but during times wherein there are large underlying moves you could see how squaring 0DTE risks through simply trading other 0DTE contracts could become difficult.

This is something we will be covering in more detail over the coming weeks.

| SpotGamma Proprietary Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Reference Price: | $4783 | $476 | $16832 | $409 | $1950 | $193 |

| SpotGamma Implied 1-Day Move: | 0.68% | 0.68% |

|

|

|

|

| SpotGamma Implied 5-Day Move: | 1.99% |

|

|

|

|

|

| SpotGamma Volatility Trigger™: | $4770 | $475 | $16620 | $402 | $1940 | $194 |

| Absolute Gamma Strike: | $4800 | $475 | $16650 | $409 | $2000 | $190 |

| SpotGamma Call Wall: | $4800 | $480 | $16650 | $409 | $2005 | $200 |

| SpotGamma Put Wall: | $4700 | $470 | $15700 | $400 | $1800 | $185 |

| Additional Key Levels | SPX | SPY | NDX | QQQ | RUT | IWM |

|---|---|---|---|---|---|---|

| Zero Gamma Level: | $4756 | $475 | $16170 | $405 | $1946 | $196 |

| Gamma Tilt: | 1.192 | 1.033 | 2.15 | 1.268 | 0.937 | 0.797 |

| SpotGamma Gamma Index™: | 1.146 | 0.033 | 0.152 | 0.146 | -0.005 | -0.04 |

| Gamma Notional (MM): | $522.725M | $175.372M | $15.909M | $676.961M | ‑$5.274M | ‑$366.675M |

| 25 Delta Risk Reversal: | -0.033 | -0.028 | -0.034 | -0.032 | -0.016 | -0.016 |

| Call Volume: | 501.536K | 1.72M | 9.366K | 910.509K | 12.639K | 425.585K |

| Put Volume: | 1.017M | 2.362M | 11.07K | 1.187M | 23.898K | 755.641K |

| Call Open Interest: | 6.356M | 6.678M | 57.066K | 5.008M | 230.047K | 4.724M |

| Put Open Interest: | 12.682M | 13.811M | 73.064K | 8.584M | 413.118K | 8.14M |

| Key Support & Resistance Strikes |

|---|

| SPX Levels: [4800, 5000, 4750, 4700] |

| SPY Levels: [475, 480, 470, 477] |

| NDX Levels: [16650, 17000, 16700, 16800] |

| QQQ Levels: [409, 410, 408, 404] |

| SPX Combos: [(5013,87.70), (4999,97.33), (4975,76.37), (4951,95.56), (4927,88.21), (4918,74.11), (4899,99.23), (4889,80.46), (4880,74.25), (4875,94.63), (4865,81.28), (4860,76.19), (4856,74.63), (4851,99.02), (4846,73.64), (4841,84.59), (4836,80.73), (4832,85.89), (4827,98.66), (4822,83.32), (4817,97.12), (4808,96.21), (4803,75.10), (4798,99.83), (4789,73.57), (4774,94.68), (4765,74.16), (4755,84.64), (4750,84.19), (4746,81.96), (4741,72.22), (4736,73.41), (4726,72.56), (4722,76.52), (4717,86.37), (4712,73.22), (4707,74.73), (4698,96.36), (4679,75.65), (4674,77.73), (4669,80.28), (4650,89.58), (4626,73.31), (4616,77.36), (4602,92.75), (4549,78.27)] |

| SPY Combos: [478.11, 488.12, 483.35, 480.97] |

| NDX Combos: [16648, 16850, 17052, 16816] |

| QQQ Combos: [405.05, 409.97, 414.88, 409.15] |

SPX Gamma Model

$3,852$4,352$4,852$5,741Strike-$1.7B-$899M-$99M$1.4BGamma NotionalPut Wall: 4700Call Wall: 4800Abs Gamma: 4800Vol Trigger: 4770Last Price: 4783

Strike: $5,089

- Next Expiration: $712,576,215

- Current: $714,617,433

View All Indices Charts