Close

Sobre Option Elements

Formación

Cursos

Unirse al Salón de Trading

Contacto

Acceso

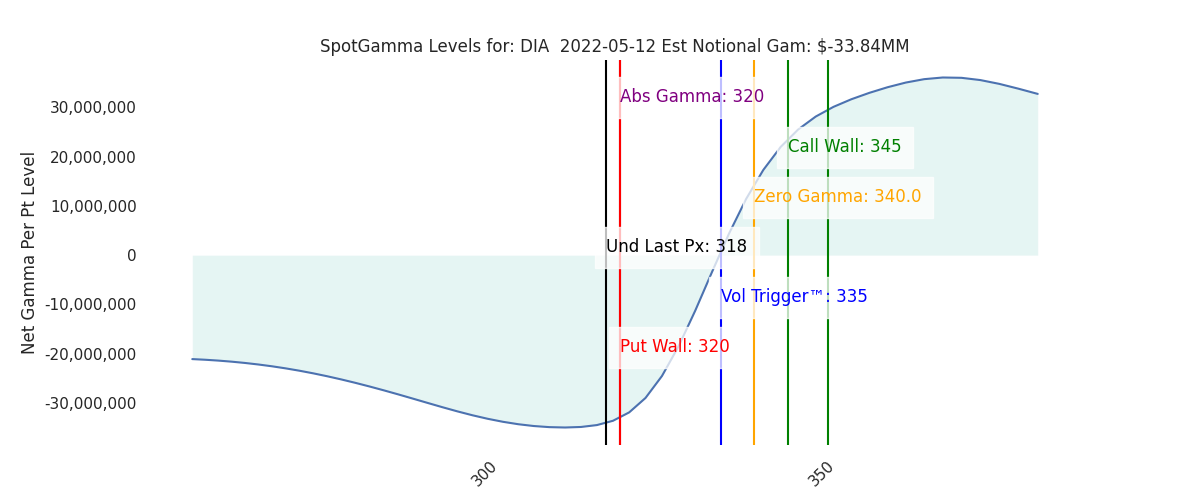

Informe SG Levels

Volver a ajustes

Usamos cookies para asegurar que te damos la mejor experiencia en nuestra web. Si continúas usando este sitio, asumiremos que estás de acuerdo con ello.

Aceptar