Futures are up slightly to 3914. We are somewhat surprised to see the SPX Call Wall jump to 4000 today, with the SPY Call Wall holding 395. This shift is the result of 15k net puts added to the 3900 strike, which increases 3900 as a floor, and confirms a higher SPX price range. For today we anticipate a tight trading range of ~60bps, with 3 major levels: 3896, 3923, and 3947.

Yesterdays intraday volatility did add a bid more weight to tomorrows OPEX, which could signal a bit more volatility next week. In particular it reduces gamma at strikes up into the 3950 range which could reduce resistance overhead.

It was only a few weeks ago that we wrote about some of the risks that we saw in markets. Primary to this was:

1) Low hedging

2) Low levels of shorting

3) High levels of levered speculation (calls + margin).

The GME saga cleared out much of this risk, for about 10 days. We can see many signs of rampant speculation in areas like “pot stocks” (ex: TLRY +50% y’day), and “short funds” are struggling. Lastly we came across this chart from the CBOE, which shows a 3 month trailing put/call ratio (total stocks, not just SPX).

We understand there are “stimulus based” bull cases for higher asset prices, and we are not here to comment on longer term, macro themes. Our models are generally tied to the “OPEX cycle” and are not intended to look out much past 4-6 weeks. Based on these notes above and this cycle we believe we can highlight periods of higher risk and volatility, which appear to be aligning post 2/19 expiration.

Macro Note:

3900-3950 into Feb OPEX

| Signal Name | Latest Data | Previous | SPY | NDX | QQQ | ||

|---|---|---|---|---|---|---|---|

| Ref Price: | 3907 | 3908 | 390 | 13651 | 332 | ||

| VIX Ref: | 21.99 | 21.99 | |||||

| SG Gamma Index™: | 1.10 | 1.20 | 0.17 | 0.03 | -0.01 | ||

| Gamma Notional(MM): | $384 | $415 | $969 | $5 | $-46 | ||

| SGI Imp. 1 Day Move: | 0.61%, | 24.0 pts | Range: 3883.0 | 3931.0 | ||||

| SGI Imp. 5 Day Move: | 3899 | 2.06% | Range: 3819.0 | 3979.0 | ||||

| Zero Gamma Level(ES Px): | 3839 | 3841 | — | 0 | |||

| Vol Trigger™(ES Px): | 3820 | 3845 | 388 | 12800 | 328 | ||

| SG Abs. Gamma Strike: | 3900 | 3900 | 385 | 12800 | 330 | ||

| Put Wall Support: | 3700 | 3550 | 370 | 11300 | 320 | ||

| Call Wall Strike: | 4000 | 3900 | 395 | 13950 | 335 | ||

| CP Gam Tilt: | 1.49 | 1.32 | 1.34 | 1.7 | 0.96 | ||

| Delta Neutral Px: | 3688 | ||||||

| Net Delta(MM): | $1,273,936 | $1,257,528 | $212,252 | $41,557 | $75,161 | ||

| 25D Risk Reversal | -0.08 | -0.08 | -0.07 | -0.07 | -0.07 | ||

| Top Absolute Gamma Strikes: SPX: [4000, 3900, 3850, 3800] SPY: [395, 390, 385, 380] QQQ: [330, 325, 320, 315] NDX:[13950, 13500, 13000, 12800] SPX Combo: [3896.0, 3998.0, 3947.0, 3923.0, 3955.0] NDX Combo: [13750.0, 13954.0] The Volatility Trigger has moved DOWN: 3820 from: 3845 The PutWall has moved to: 3700 from: 3550 The Call Wall has moved to: 4000 from: 3900 SPX resistance is: 4000. Support is: 3900 .Reference ‘Intraday Support’ levels for support areas. The total gamma has moved DOWN: $384MM from: $415.00MM Gamma is tilted towards Puts, may indicate puts are expensive Positive gamma is moderate which should lead to smaller market moves. Average Range on day is 1.5% |

| Sub Login Follow @SpotGamma Strike Charts Historical Chart Gamma Expiration Tool |

| ©TenTen Capital LLC d.b.a. SpotGamma Please leave us a review: Click Here |

| See the FAQ for more information on reading the SpotGamma graph. |

| SpotGamma provides this information for research purposes only. It is not investment advice. SpotGamma is not qualified to provide investment advice, nor does it guarantee the accuracy of the information provided. This email is intended solely for subscribers, please do not distribute the information without the express written consent of SpotGamma.com. |

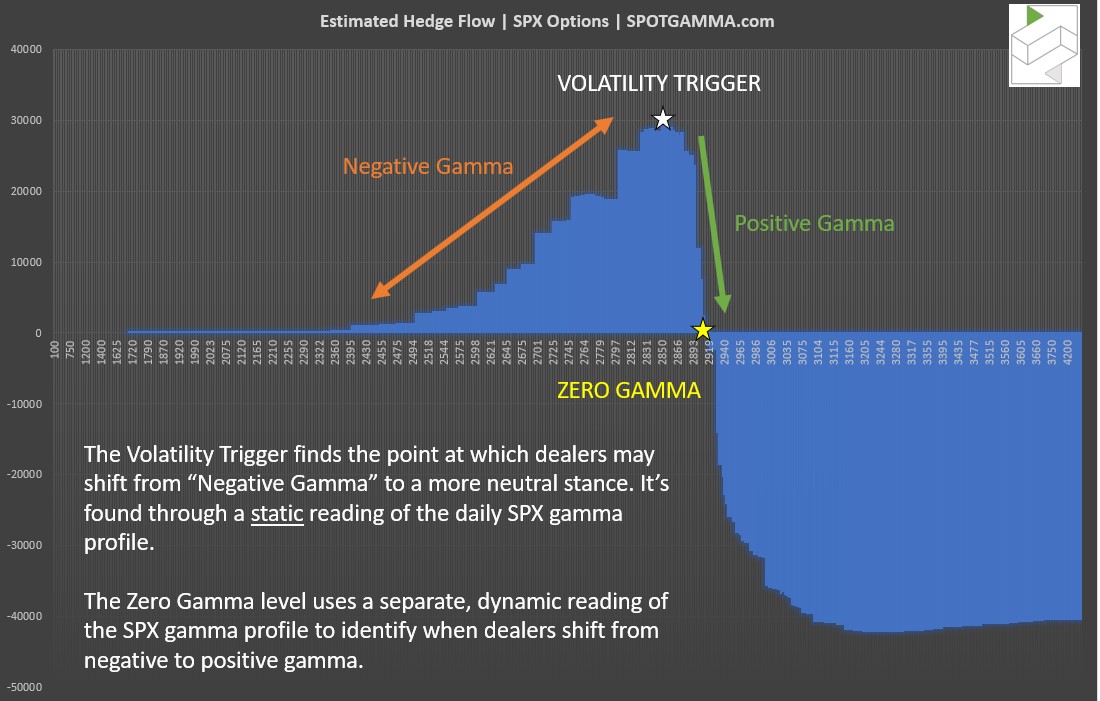

| SPX Ref: Estimated ES Futures price at which data was run. VIX Ref: Estimated VIX price at which data was run. SG Gamma Index: Proprietary gamma modeling index value. Combo Strike™: A combination of SPY/SPY open interest, then “price normalized” back to the SPX Gamma Notional: Estimated amount of notional gamma based on traditional gamma modeling. SG Imp. 1SD Move: For one day ahead it is the projected 1 standard deviation SPX move implied by the SG Gamma Index. High Gamma Strike: Strike with the highest level of net positive gamma. Seen as a resistance level. Top Absolute Gamma Strike: Level with most call gamma + put gamma. Zero Gamma Strike: Estimated level at which gamma flips from positive (above strike) to negative (below strike). Volatility Trigger™: Similar to Zero Gamma in that its a level at which dealers may shift from positive (above trigger) to negative (below strike). Click here for a Zero Gamma vs Volatility Trigger Diagram Put Wall Strike: Strike with largest level of put gamma. Seen as a general support area. CP Gamma tilt: Call gamma to put gamma ratio. Extreme readings may show skewed investor sentiment. Delta Neutral Strike: Estimate where the options market may price the delta neutral level. This is NOT model adjusted meaning that we make no assumption on dealer positioning. 25 D Risk Reversal: A measurement of the 25 delta call minus 25 delta put on a ~30 day rolling basis. Used to measure call values relative to puts. |

{kind=link}