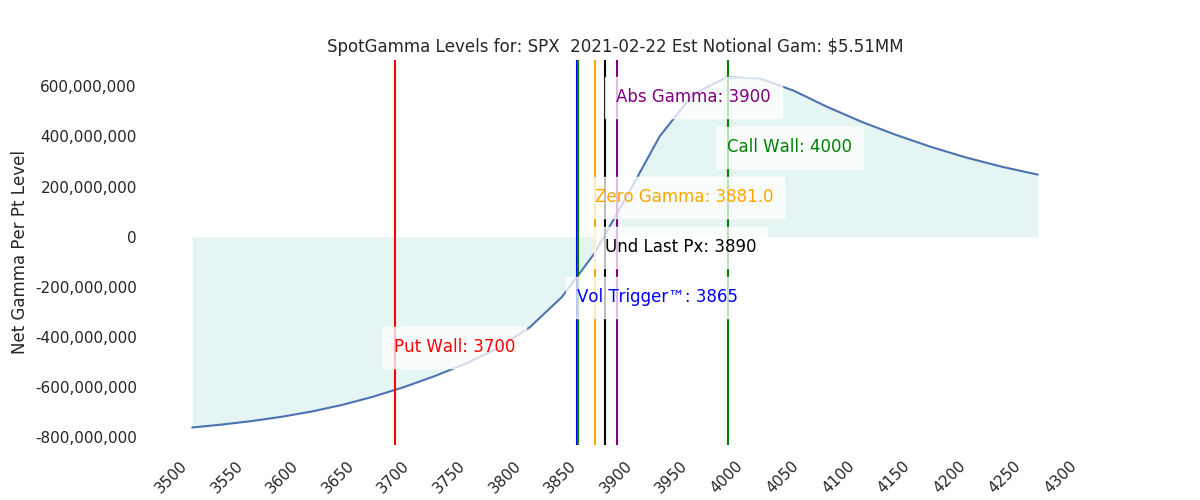

Futures are down from Friday near the 3875 level. Notional gamma levels are zero for S&P500, and negative for QQQ/NDX and RUT/IWM. This implies high volatility and a larger directional move today. The Volatility Trigger (our critical risk line) stands at 3865, with appeared to hold as overnight support. 3900 remains as the largest options strike on the board, and key resistance. To the downside we watch 3850 as initial support, and 3800 as major support.

The key directional signal today may be the implied volatility (ie VIX). If the VIX pushes higher that can signal demand for put options which infers dealers may have to sell ES futures to hedge. Of course a VIX drop could signal dealers have ES futures to buy. These are the mechanics that can help propel larger directional moves.

Last week we talked about realized volatility which is still in decline after last weeks “pin” to 3900. If this metric continues to compress it should place pressure on implied or future volatility expectations. However it seems that current SPX/SPY implied volatility prices are diverging and shifting higher as we talked about on Friday.

We mention these metrics again as now that markets hold flat to negative gamma “realized” volatility could expand again and start syncing with those higher implied volatility expectations. This does not have to express as a quick drawdown (though it could), it could also reflect a quick run to 4000.

Macro Note:

March OPEX range TBD

| Signal Name | Latest Data | Previous | SPY | NDX | QQQ | ||

|---|---|---|---|---|---|---|---|

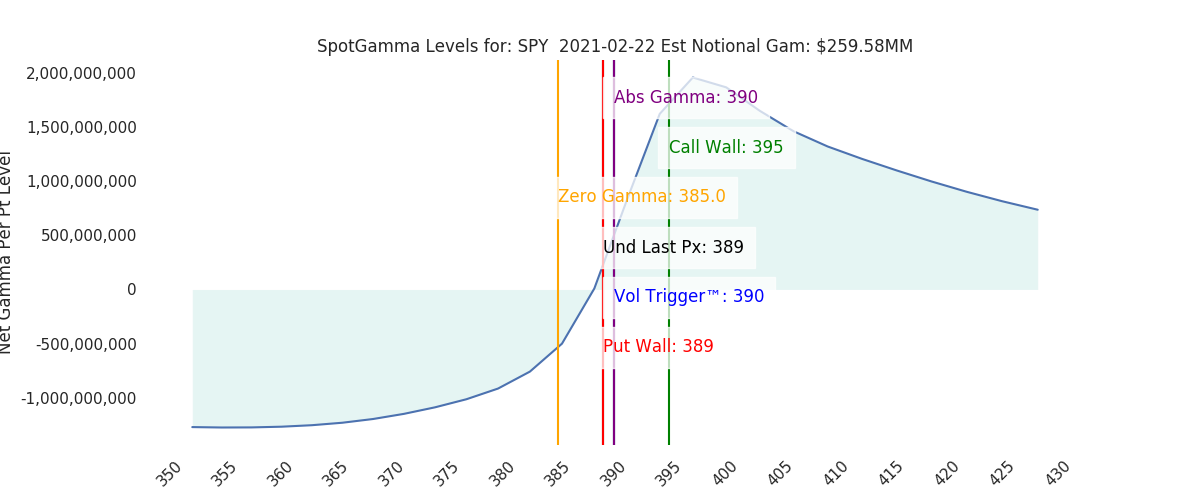

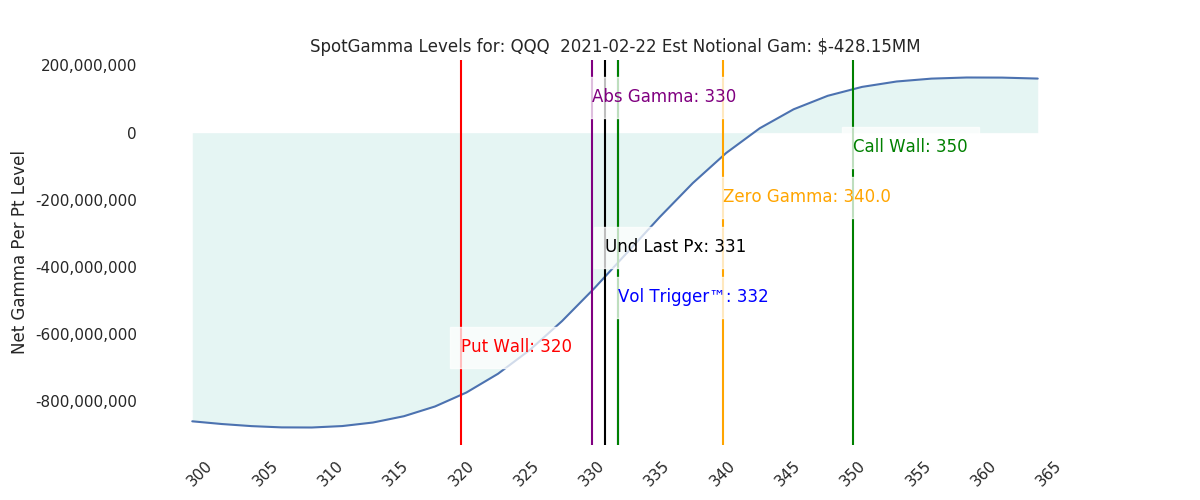

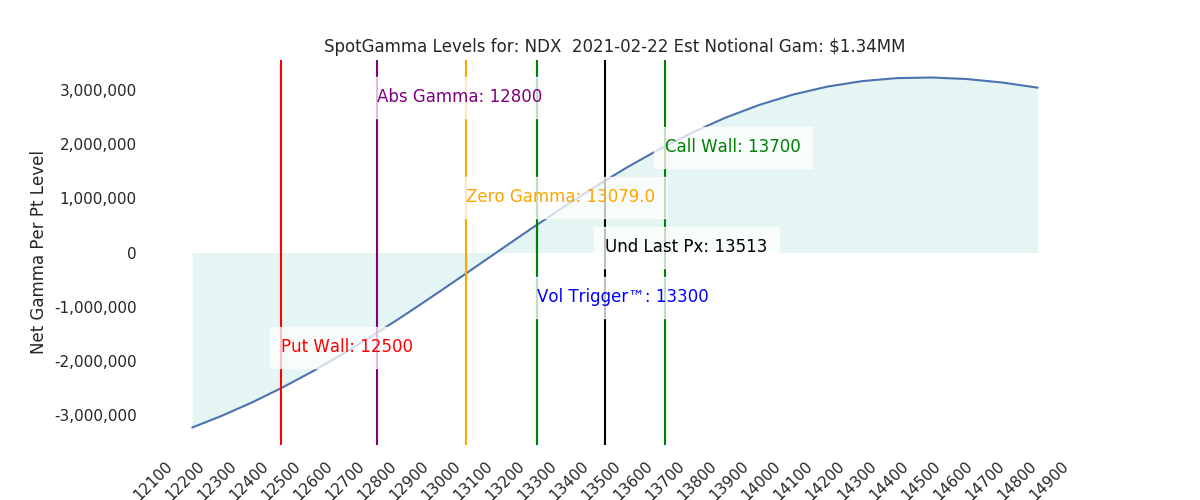

| Ref Price: | 3890 | 3908 | 389 | 13513 | 331 | ||

| VIX Ref: | 14 | 22.02 | |||||

| SG Gamma Index™: | 0.50 | 0.87 | 0.08 | 0.01 | -0.07 | ||

| Gamma Notional(MM): | $6 | $161 | $260 | $1 | $-428 | ||

| SGI Imp. 1 Day Move: | 1.18%, | 46.0 pts | Range: 3844.0 | 3936.0 | ||||

| SGI Imp. 5 Day Move: | 3890 | 2.08% | Range: 3810.0 | 3971.0 | ||||

| Zero Gamma Level(ES Px): | 3881 | 3869 | — | 0 | |||

| Vol Trigger™(ES Px): | 3865 | 3840 | 390 | 13300 | 332 | ||

| SG Abs. Gamma Strike: | 3900 | 3900 | 390 | 12800 | 330 | ||

| Put Wall Support: | 3700 | 3700 | 389 | 12500 | 320 | ||

| Call Wall Strike: | 4000 | 3950 | 395 | 13700 | 350 | ||

| CP Gam Tilt: | 1.19 | 1.09 | 1.09 | 1.16 | 0.63 | ||

| Delta Neutral Px: | 3728 | ||||||

| Net Delta(MM): | $1,213,164 | $1,345,958 | $190,265 | $38,310 | $68,447 | ||

| 25D Risk Reversal | -0.09 | -0.07 | -0.09 | -0.09 | -0.1 | ||

| Top Absolute Gamma Strikes: SPX: [4000, 3900, 3850, 3800] SPY: [395, 390, 385, 380] QQQ: [330, 325, 320, 315] NDX:[13750, 13700, 12800, 12500] SPX Combo: [3986.0, 3936.0, 3959.0, 3912.0, 3932.0] NDX Combo: [13277.0, 13886.0, 13683.0, 13642.0] The Volatility Trigger has moved UP: 3865 from: 3840 The Call Wall has moved to: 4000 from: 3950 SPX resistance is: 3900 .Reference ‘Intraday Support’ levels for support areas. The total gamma has moved DOWN: $6MM from: $161.00MM Gamma is tilted towards Puts, may indicate puts are expensive Positive gamma is moderate which should lead to smaller market moves. Average Range on day is 1.5% |

0 comentarios